A Sweet Spot in a Complex Web

What the market liked in Eternal's results & what investors should look for next?

Eternal (formerly known as Zomato) is becoming a very complex stock to track, with multiple moving parts due to the various businesses it is present in:

Maturing food delivery business, Zomato

Accelerating growth (along cash burns) in QCom vertical, Blinkit

Latest offering on going-out with a huge potential, District

B2B supplies which is acting like a backbone, Hyperpure

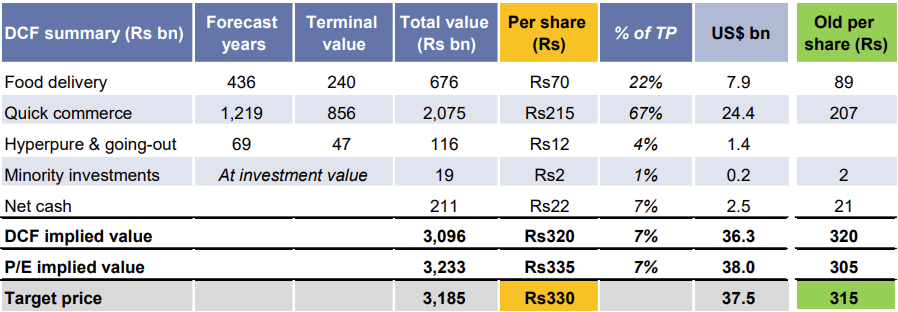

Amidst all this, another key issue in tracking Eternal is that things move very fast within the company, thanks to superb execution. For example, the value of Blinkit has literally gone up 45 times in just the last 3 years, from ~Rs 4,500 Crores to an estimated ₹2,07,500 crores as of mid-2025 (ie Rs 2,075 billion as shown in table below). At the time of acquisition in 2022, this quick commerce arm was not even 10% of Eternal’s market cap. But as of 2025, it contributes roughly 70% of the current market cap, according to analyst estimates like those from Goldman Sachs.

Similarly, their going-out experience vertical, District, currently contributes less than 4% to the market cap. However, the District team, led by Rahul Ganjoo, has guided toward tripling their annual topline (NOV) to $3 billion and achieving an adjusted EBITDA of $150 million within the next five years. If they manage to execute this in a shorter time frame, say within the next 2 to 3 years, the market could start assigning significantly more value to this vertical as well.

Therefore, for any analyst on Dalal Street, it’s incredibly hard to predict what this company will look like just five years from now. Forget about estimating the terminal value, lol! The teams within the firm compete fiercely, and their execution outcomes speak for themselves.

“We want to keep our heads down, and keep up the momentum in solving problems for our customers, without having or needing to look back to see how far we have come.”

Considering multiple moving parts, a lot of investors I know form their opinions about the results based on the stock’s reaction afterward, because complexity of the business has constantly increased overtime. So for writing today’s blog, I went through all the research notes from Dalal Street analysts who track this stock. I'm bringing to you a few key factors from the results that were clearly liked by the market, and what you should watch for next as an investor in the stock.

If you’ve been reading my blogs here at Finding Outperformers for a while now, you might have come across our past research on Eternal here and would know how bullish I’ve been on the stock - just putting that disclaimer upfront.

In case you find today’s blog useful, do like it and share your feedback in the comments below. Let’s get started!

Market desperately needs ‘New Leaders’

As the Q1 results for Financial Year 2026 come out, we are witnessing one of the worst earnings seasons since COVID, with flat toplines, falling margins, and consequently, pressure on profits. India’s services export backbone, the IT majors like TCS, Infosys, Wipro, and HCL, are facing existential questions in the age of AI. Giants like Reliance are struggling to show organic growth, while banks and NBFCs (except HDFC and ICICI) are hinting at stress, with even market darlings like Bajaj Finance facing analyst downgrades. Some of the highest-growing companies like Trent are also failing to meet expectations and are seeing downgrades.

In such a scenario, when blue chips are struggling and growth is becoming scarce, the growth premium tends to rise for stocks that are able to deliver decent results, as the market is always eagerly looking for the leaders of the next rally. Eternal is becoming one of those stocks that returned to the limelight. Its revenue from operations in Q1FY26 stood at ₹7,167 crore, up 70.4% from ₹4,206 crore YoY, led by Blinkit, which is growing at 140% YoY. Along with strong growth, management commentary was stronger than expected on margins front along with lower burn, which led the stock to jump 20% post results to a fresh all-time high.

I had talked about the possibility of such a surprise in Eternal’s Q1 results back in May 2025 in my LinkedIn post here, where I mentioned that the management had already cautioned the street quite significantly. This had lowered market expectations and opened up the possibility for a positive surprise in the results. That is exactly what happened, and the stock was at an all-time high post results.

Market hates Cash Burn!

Eternal had started generating some positive cash inflows on a quarterly basis about two years ago, but that trend reversed in the last two quarters (Q3 and Q4 of FY2025), when the company reported a net cash burn (i.e., cash reduction).

This improved again in the Q1 FY2026 results, with the company managing to arrest the cash burn and posting a small positive cash balance of ₹33 crore. While this amount might appear small for a company with quarterly revenue of over ₹7,000 crore, and is all due to ‘other income’, it's important to note that as of March 2025, the quick commerce industry had a cash burn rate of Rs 5,000 Crores on quarterly basis. Blinkit, with a 40% market share in that industry, is operating in a space where conserving cash is a significant achievement.

Therefore, the reduction in cash burn across the quick commerce industry, led by challenges faced by rival Zepto (which delayed its IPO plans due to poor unit economics), has turned out to be a big positive for market leader Blinkit. According to Datum Intelligence, the daily active users for both Zepto and Blinkit were 5.5 Mn in December 2024. In June 2025, this number reduced to 4.9 Mn for Zepto, but rose to 6.2 Mn for Blinkit and a similar trend continued in July 2025 as well.

Market was also concerned after Swiggy’s Q4 FY25 results, where it reported a cash burn of ~Rs 1,500 Crores in just 3 months. However, it’s been quite a u-turn with competitive intensity now reducing, better days are anticipated for quick commerce platforms.

[Eternal may need to use a portion of its ₹18,900 crore cash balance (as of June 2025) to own inventory in Blinkit due to a model shift, this is largely on expected lines]

Change in Commentary on Margins

One of the key negative highlights of the Q4 FY2025 (and even Q3 FY2025) results was the management’s cautious commentary around margins, driven by persistent competitive intensity in the quick commerce space. However, with a noticeable reduction in aggression from Zepto, the number two player after Blinkit as mentioned above, there was a significant shift in tone in the Q1 FY2026 shareholder letter.

Take a look at the two statements below to see how the management’s guidance has changed:

“In the absence of competition, we would have expected the business to be fairly profitable by now. And all of that is what is not reflecting in the P&L because of high competition.”

- Akshant Goyal, CFO, Eternal

Just 3 months later, in Q1 FY2026 Shareholder Letter

“As far as near-term is concerned, it does feel like % margins have bottomed out and, if the competitive environment stays the same, we should see margins getting better from here…”

- Akshant Goyal, CFO, Eternal

Therefore, a clear guidance that margins would improve going forward due to a reduction in competitive pressure came as a positive surprise for the market. On top of that, the management stated there will be a “100 basis point contribution margin expansion over the next 2 to 3 quarters” driven by a shift in the business model, from third-party ownership to a self ownership model for inventory where the company owns the inventory on its books.

Add to it another 100 basis point improvement from operating leverage and reduced competition which the street is now anticipating, implying a total contribution margin expansion of 200 basis points by the end of FY2026! An industry were margins are wafer thin, a 2% (ie 200 basis points) improvement is a big positive, especially at the scale at which Eternal operates.

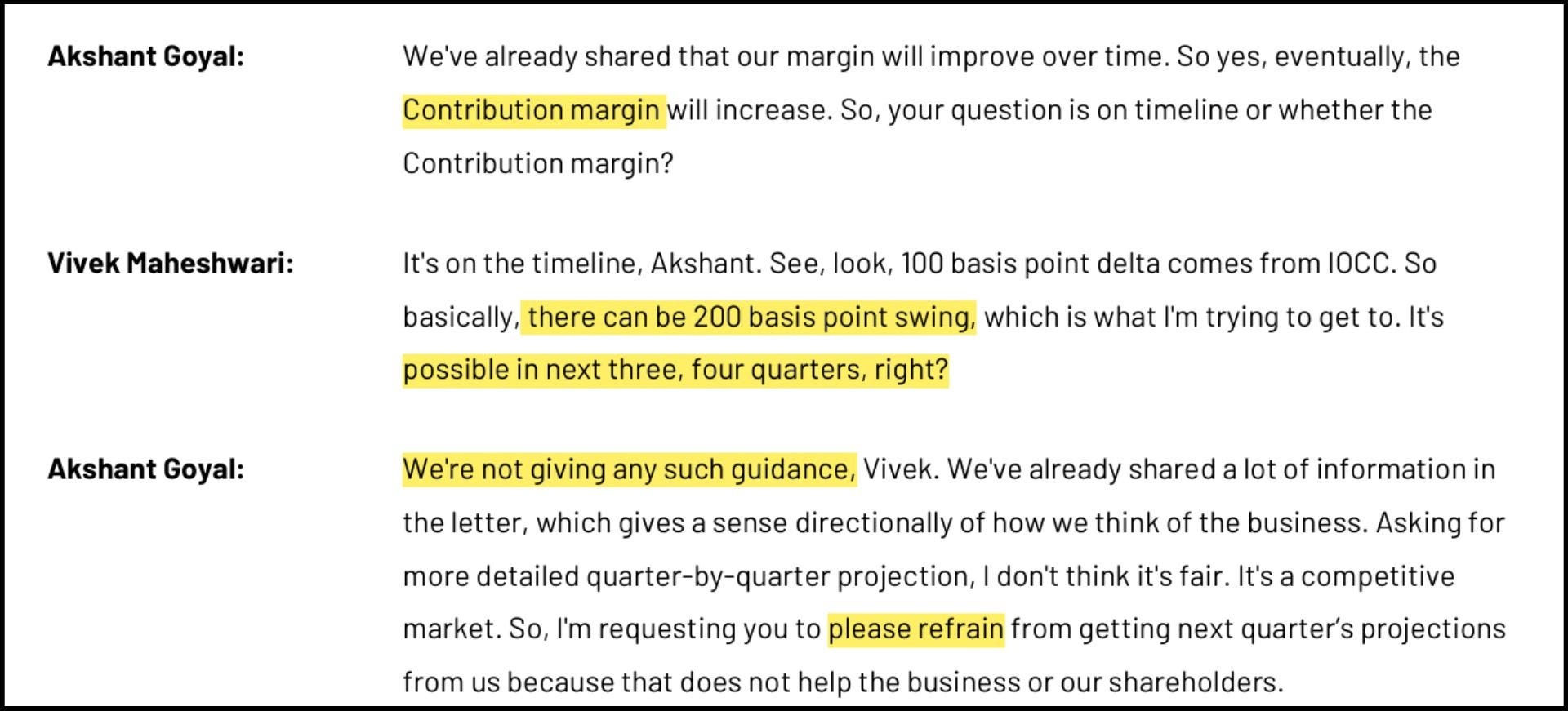

In an interesting instance during the concall, analyst Vivek Maheshwari (Jefferies) raised a question about this, to which Akshant (CFO) asked him to refrain from asking such questions. Read the extract below:

Now, I’m sure this 200 basis point contribution margin improvement possibility in short term caught the attention of all street analysts, as no one was expecting the bull case scenario to be that strong, even though the management has not confirmed it.

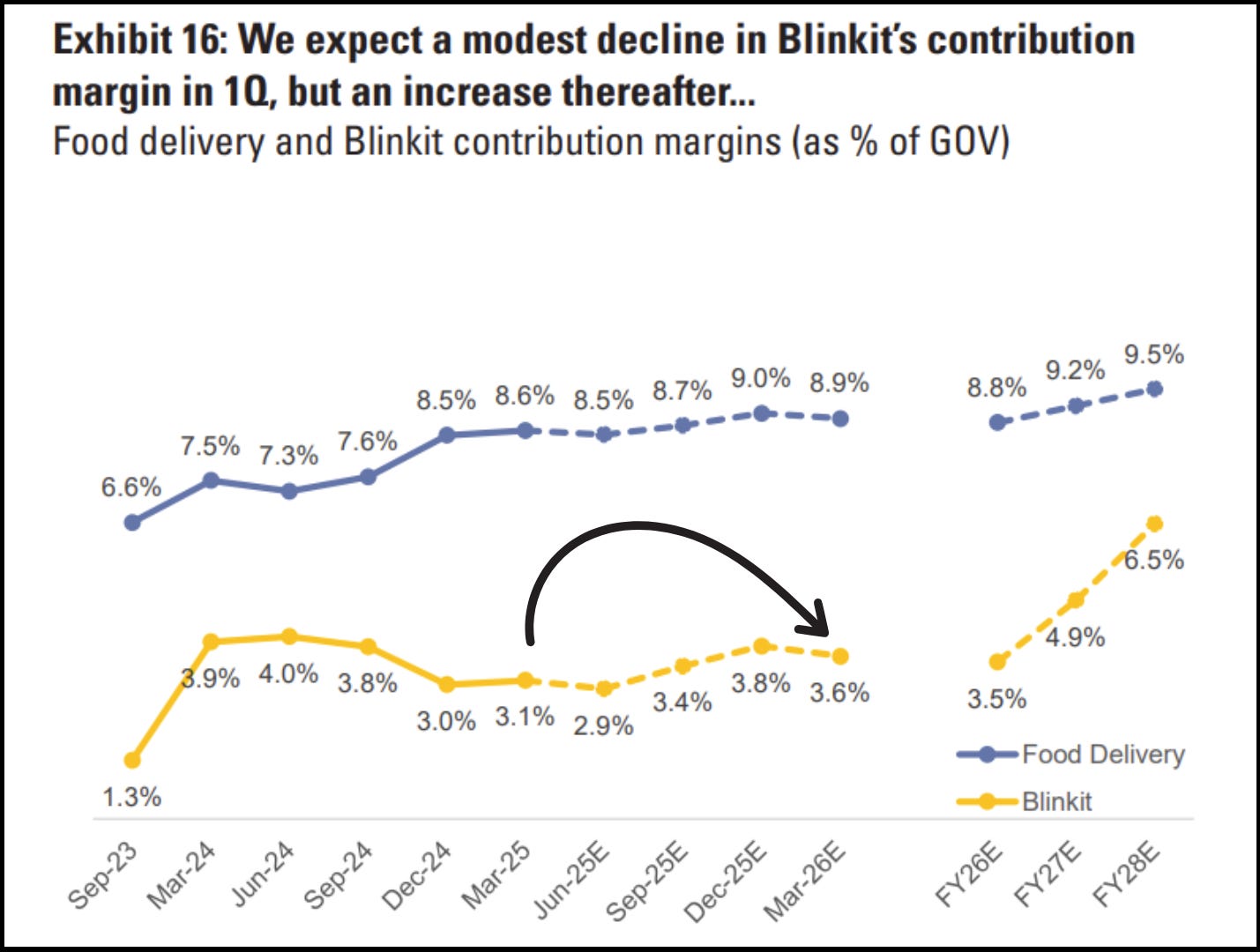

Take Goldman Sachs’ estimates as of July 2025, before the Q1 FY2026 results. They projected Blinkit’s contribution margin to rise from 3.1% in March 2025 to 3.6% by March 2026, implying only a 50 basis point improvement.

Clearly, there is a gap between what the street was expecting and what could be playing out which made the share hit a fresh high. JP Morgan’s analyst quietly raised their contribution margin estimate to 4.5% by March 2026 for Blinkit (which they earlier anticipated at 4%), implying a 150 basis point improvement in their base case. Jefferies also increased their target price by 60%, stating that they had 'overestimated' the competitive threat while giving a Buy call on the stock.

Evidence of larger TAM visible

While the year 2024 was an eye-opener for the market in terms of the categories of products that can be served by the quick commerce (Qcom) industry, the year 2025 could emerge as an eye-opener on the potential for Qcom to succeed in small towns as well, while continuing to hold up on the unit economics front.

One key concern for investors has been that the Qcom industry is limited to the top 8 cities, where population density and incomes are higher, making the business model economically viable. These factors are not as strong in Tier 2 and beyond cities, leading to doubts about Qcom's scalability outside Tier 1.

But that may not be entirely true. Here is what the management had to say:

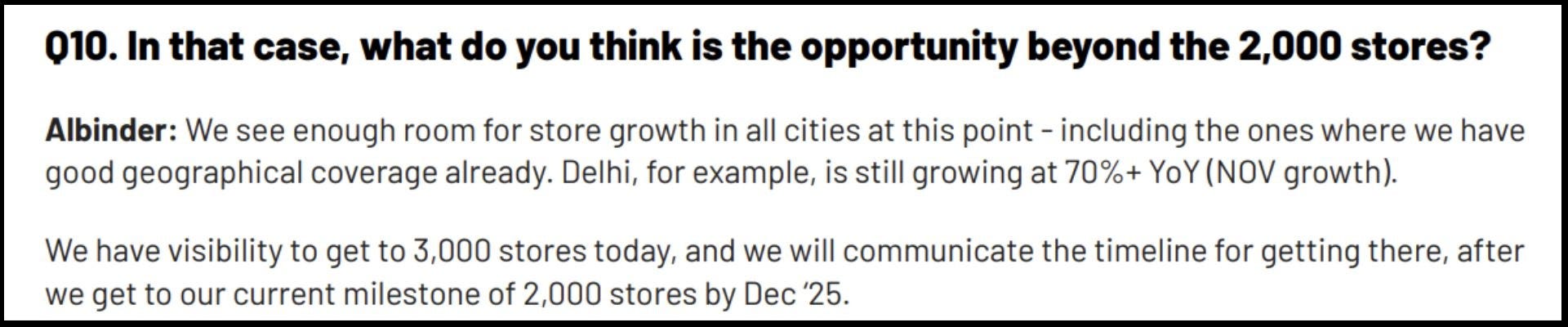

“Smaller cities are equally promising as far as profitability is concerned. The difference in Net AOV (NAOV) of our large and small cities is fairly narrow at ~10%. Hence, after accounting for lower cost of operations in smaller cities, there is early evidence that margins will be attractive even in smaller cities.”

Outcome? Blinkit has given a new store count guidance of 3,000 stores, up from earlier guidance of 2,000 stores.

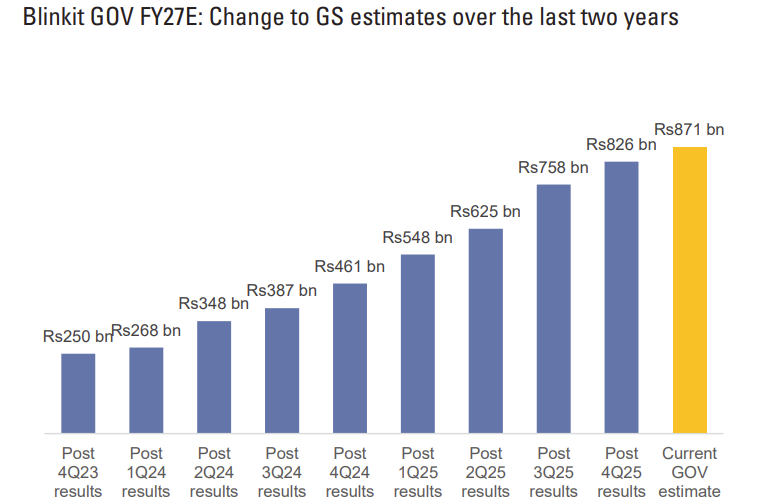

While analysts have been consistently raising Blinkit’s revenue and GOV estimates quarter after quarter over the last two years, unit economics now being proven in Tier 2 cities and beyond opens up further scope for upward revisions, as the total addressable market continues to expand.

What next to watchout?

As Blinkit continues to surprise on the growth front, this may no longer be a key trigger for any further up move in the stock, as the street has now come to expect consistent topline beats. The next key surprise in the short term is clearly around Blinkit’s profitability margins. Eternal has a golden opportunity to emerge as a leader within the Nifty 50 stocks in the next bull run. If it can improve its margin profile faster than expected and start generating strong cash flows, the street would take notice.

In the medium term, as I mentioned above, the next big surprise must come from a vertical other than Blinkit. District appears to be the most promising candidate at the moment, where market estimates are assigning it less than 4 percent of Eternal’s overall value. Initiatives like Nugget are exciting in terms of future potential, but for the street to consider them meaningful, a real breakthrough proving product-market fit will be required.

I shall continue to track all aspects of the company closely as its my biggest holding. Connect with me on LinkedIn here.

Finding Outperformers will always remain a free-to-access website. If you find our work valuable, consider supporting our team by contributing to our research here:

Read our past publications on Eternal (Zomato):

Why Zomato needs an AWS moment?

Shifting gears from operational-heavy businesses to a tech-led model

Disclaimers-

We are not a SEBI registered advisors; personal investment/interest in shares can exists for any company mentioned above; this isn’t investment advice but our personal thought process; DYOR (do your own research) is recommended; Investing & trading are subject to market risk; the decision maker is responsible for any outcome.

Great read, as always! Keep up the good work

Worth Reading. Thanks for sharing Aditya.