DMart: Cracking the Retail code

Why Avenue Supermarts is a superb choice to play the consumption theme

This is my 3rd blog on the ‘Playing the Consumption Story of India’ series after Titan (link here) and Eicher Motors (link here). In these 2 blogs, I focused on how India’s Macros are shaping up with private capex finally lifting off by companies that are at their lowest debt levels in a decade. We also discussed India’s rich demographics that shall support consumption in the medium to long term, whereas in the short term, we have the crores of spending in the General elections of 2024 lined up that can boost overall consumption levels in 6 months before & after the elections. In this 3rd blog of mine, I discuss how I finally ended up buying Avenue Supermart (which is the parent entity of DMart; used interchangeably with DMart in this blog) shares recently with an outlook to acquire shares more in the coming months.

Note: If my emails end up in the ‘promotions’ tab, please move them to inbox so you don’t miss out. Don’t forget to subscribe and join 350+ readers!

How DMart started & competition landscape

In the early 2000s, Radhakishan Damani, one of India's most prominent and influential investors, made a pivotal decision to step away from the stock market and venture into the retail business. He drew inspiration from Walmart's successful deep-discounting and cost optimization model, which emphasized providing the best quality products to customers.

In the following years, several big players, such as Big Basket, EasyDay by Future Group, Best Price by Walmart, METRO Supermart, Reliance Retail by Reliance, and more, entered the retail market. The sector saw an influx of thousands of crores of investment and debt in the two decades after Dmart's launch.

The outcome? Future Retail, a once-prominent entity, is now facing bankruptcy, burdened with over Rs 30,000 crores in overall debt to be repaid to its lenders. This serves as a stark contrast to Dmart's success and efficient business approach under Radhakishan Damani's leadership. Best Price by Walmart was acquired by Flipkart (owned by Walmart) (link) & has not really expanded after initial success with just ~30 stores in India yet. METRO sold its Cash & Carry stores to Reliance (link) for Rs 2850 Cr and exited the Indian market. Reliance Retail continues to grow strong; already having the largest number of stores and tapping all acquisition opportunities possible.

The market dynamics underwent significant changes due to COVID, with a greater emphasis on e-commerce, particularly quick-commerce. New players like Blinkit, Swiggy Instamart, Zepto, and even JioMart have introduced fresh dynamics to the retail business model, which prompted DMart to shift its focus towards online orders after the pandemic.

However, these venture capital-backed players are currently facing a funding crunch, as the era of cheap money ended with an increase in rates starting from 2022. As a result, players like Dunzo have been forced to close over 70% of their dark stores, due to poor economics per store. This situation highlights the challenges and adjustments faced by the retail industry as it adapts to the evolving market conditions post-COVID.

Where does DMart stand today?

DMart today stands steady and expanding at a decent pace; here is a graph from Motilal Oswal’s analyst report showing how their stores have grown over the years which today stand at 330 as I write this blog:

As of today, ~50% of their stores are concentrated in Gujrat & Maharashtra region (which was ~60% a few years ago) and don’t have a presence yet in about 2/3 states of India. Moreover, they never spend on marketing and that is the reason why people from North and Eastern states in India have often never heard about DMart stores. Another reason why they haven’t exploded their number of stores is because of their business model where they aim to own the land wherever they open their stores rather than taking it on rent. Such a business model requires a lot of capital either in the form of debt or equity. DMart does not take loans to expand but rather invests back all its profits into its business to fuel store expansion.

But why now?

The story of DMart is well-discovered. Being an institutional stock, it has a wide coverage base which definitely knows a lot more than me when it comes to investing in this stock. Then why do I begin to invest in my portfolios today?

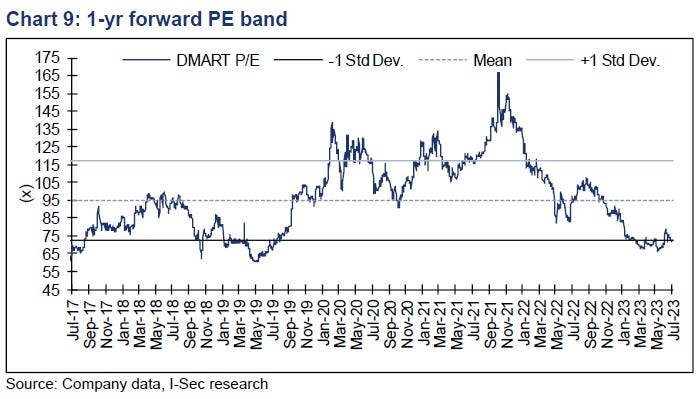

To be honest, I have been looking to invest in Avenue Supermart shares for a few months now. Being in love with the story, and actively looking to invest more in consumption themes, what makes me more comfortable today to invest is the valuation at which the shares trade today. Here is a chart explaining my confidence today:

^This chart illustrates the 1-year forward price-to-earnings (PE) band of DMart, indicating that the premium valuations the company has experienced over the past 3 years have now returned to more normal levels. Back in 2017, when Mr. Damani launched the IPO of Avenue Supermart at Rs 300, it opened at Rs 600 on Day 1, and the valuation multiples the company enjoyed at that time are comparable to the ones it is currently trading at. As depicted in the chart, the current multiple is 1 standard deviation below the average valuation the share has commanded since its IPO.

Here is another chart from recently published Morgan Stanley’s India Consumer - Valuations et al - July’23. This graph shows that the premium multiples DMart stock has been enjoying over the Sensex index, in the past 3 years, have significantly normalized over the last 1 year to the levels seen around 5 to 6 years ago; hinting towards the fact that shares are not at an overbought level now:

Adding a technical view here, the levels of ~Rs 3300 are acting as a strong base for the shares, and the shares have taken support at those levels twice in the last 2 years. Before that, the same level was a resistance level for the shares which broke on the upside in Aug’21 and made an all-time high of ~Rs 5,800

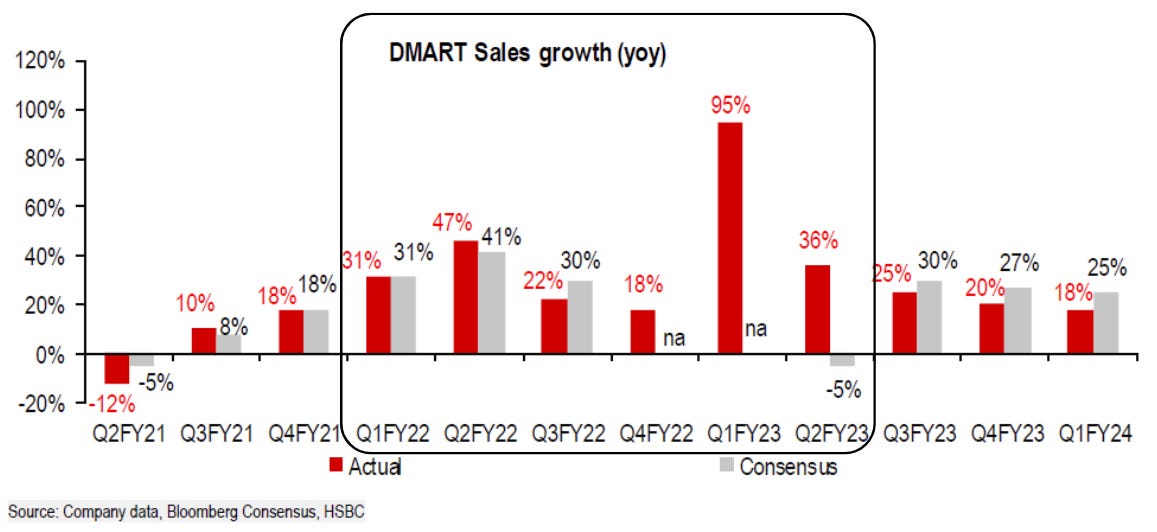

The exuberance witnessed in the shares of DMart is clearly visible from the second half of 2021 where the shares just doubled in a time span of ~3 months. While trying to understand why shares rocketed so much in 2021, I got a chart by HSBC’s analysts covering DMart showing how the company had mostly beaten street estimates in over 1.5 years by a big margin! Have a look at the Sales growth chart (analyst expectations/ actual growth):

Besides the charts, I genuinely believe that Mr. Damani is playing a long-term game to capitalize on this lucrative opportunity in front of us. What impresses me the most is their unwavering focus on the unit economics of their stores. Interestingly, I recently discovered that people today consider having a DMart nearby as an important factor when selecting a home. Although I haven't personally visited a DMart since they are not widely available in North Indian states, I watched several vlogs on YouTube to gain insights before writing this blog :)

The potential for growth is enormous, and the current market situation, such as the bankruptcy of Future Retail, foreign players exiting the market, and the funding challenges for startups, presents a great opportunity to expand this simple yet efficient business that people love to visit repeatedly.

In summary, Mr. Damani's long-term vision and dedication to unit economics position DMart well for the future. The increasing consideration of having a DMart nearby while choosing a home speaks to the strong reputation of the brand. With the market void created by recent events, DMart has an excellent chance to build on its success and further expand its customer-centric retail model.

Some Risks

Low Free-float: Approximately 75% of DMart is held by the promoters, which could lead to excessive volatility in the stock and a higher beta. Researchers may use a higher discount rate in their valuation models due to this higher beta. While there's a chance the promoter may sell some stake to improve the free float, it seems unlikely as Mr. Damani seems to have a long-term vision for the company.

India’s Retail market slowdown: One potential risk for DMart investors is a slowdown in demand for fast-moving consumer goods (FMCG) products, as the company primarily sells daily usage items. A macro-level slowdown in demand in India or a slower GDP growth rate could have a significant negative impact.

Rich valuation: DMart is currently trading at a high valuation, and FMCG stocks, in general, are not cheap either. A decrease in the valuation multiples that FMCG stocks command, which is often linked to the overall economy, poses a potential risk.

Competition from Reliance: DMart's appeal to customers lies in the competitive prices it offers on products, resulting in cost savings for buyers. However, if big players like Reliance enter the market and focus on heavy discounting, it could affect DMart's margins. The company already operates on low margins due to the nature of its business, with an EBITDA margin of around 8.5%.

That’s all for this blog, thank you for reading!

Note- Various analyst reports have been referred to in this blog, and due credits/ mentions have been given.

Disclaimers-

Personal & client investment/interest in the shares exist; this isn’t investment advice; DYOR (do your own research) is recommended; Investing & trading are subject to market risk; the Decision maker is responsible for any outcome that this Indian market