Happiest Minds, a long term multibagger?

Best placed Indian IT company today

Happiest Minds has been the investor’s favorite ever since its IPO which came at Rs 166 in 2020 & the stock price is over 6 times today in a matter of 2 years! Strong management led by founder Mr. Ashok Soota, comes with a legacy as a pioneer in the Indian IT sector.

A little background before you read on….

Before starting Happiest Minds, Mr. Ashok Soota served as the president of Wipro Infotech & was also the co-founder of Mindtree. Where Wipro grew from $2 Mn to a whopping $500 Mn revenue run rate in his term of 15+ years, Mindtree is again a multi-bagger with no revenues in 1999, to $1 Bn revenues today. It's remarkable to note that Happiest Minds IPO was oversubscribed 151 times in 2020, something similar to what his previous company Mindtree did in 2007 (Mindtree's IPO was 100+ times oversubscribed!).

Recently, Happiest Minds came out with fundraising plans of Rs 1,400 Cr which is more than 11 times higher than the amount raised by the company at the time of IPO as the fresh issue.

In this post, we shall talk about short-term & long-term strategies of the company along with how the company can perform compared to its peers with the motive to find our next outperformerrrrrrrr!

Is Happiest Minds well-placed in the near term?

In the times in which we live today, it’s tough to determine whether the IT sector as a whole is completely out of the woods yet or not. On the demand side, IT companies are facing a global slowdown & on the supply side, they are facing high attrition rates leading to an impact on their profit margin and causing a stock slump.

Even the share price of Happiest Minds is down from its peak by about 33%!

But as it’s always said that the best time to buy a share is in a crisis, so here are some facts-

A weak rupee against the dollar is a big positive for IT companies which we believe is yet to play out. The rupee was strong till it didn’t break the psychological mark of Rs 80/$, but once that was crossed, coupled with negative news in form of an OPEC Oil production cut of 2 million barrels a day & non-inclusion of Indian bonds in the world bond index in 2022 have opened the doors for further Rupee depreciation, especially against the dollar.

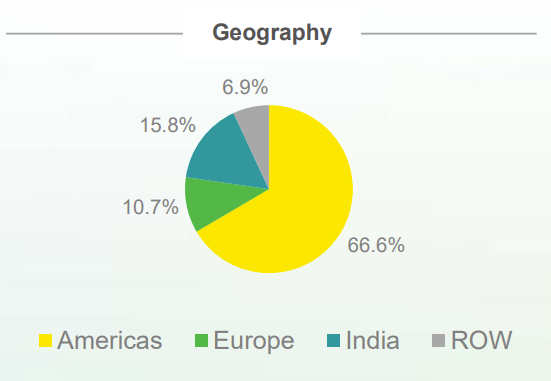

Out of the total revenues earned by Happiest Minds, 67% comes from the USA, 16% comes from India & just 11% comes from Europe which is much lesser than the likes of TCS & Wipro who earn around 30% of revenues from Europe.

Europe being the weakest market of all 3 above-mentioned geographies, the short-term outlook for Happiest Minds is surely positive relative to its peer till the European economy comes back from the crisis and troubles it is in currently.

How is Happiest Minds placed in the long term?

During their Q1 FY23 results conference, Mr. Ashok Soota stated, “Our 10-year vision statement is to be a billion-dollar company by 2031. In line with this, based on the growth we are experiencing and continued demand for digital services.”

The firm has also raised its revenue guidance for FY23 to 25% and to target compounded annual growth of 25% over the next 5 years, which could come from organic/inorganic route

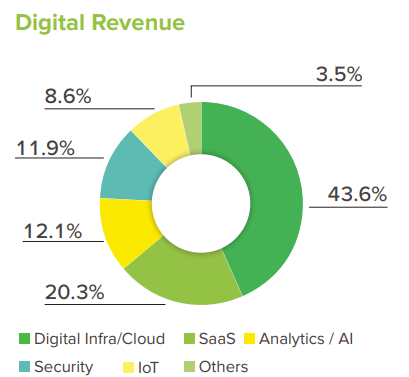

Digital Revenue Split: It’s interesting to note that along with Digital Infra/Cloud, its other major drivers of revenues, which are SAAS, Analytics/AI & Security (~ 45% of total revenues), are the ones that are the fastest growing segments within the overall IT segments and very different from the likes of TCS & Infosys who still earn a major chunk of their revenues from traditional IT & business process management services.

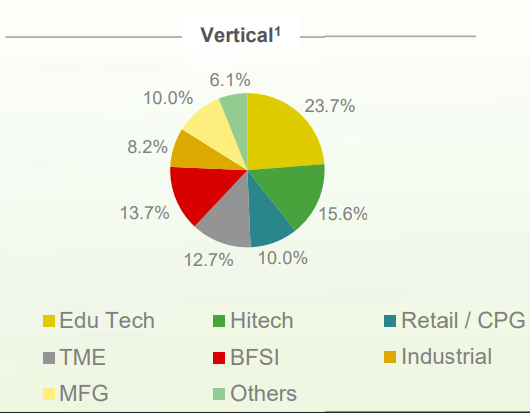

Customer Vertical Split: Here again, fast-growing tech-based segments like Edu tech & Hi-tech constitute over ~ 40% of their revenues, very different from traditional IT companies where 40 to 60% of revenues come from traditional industries like BFSI(financial sector) & Retail.

Interesting fact- Here’s an 11-year-old video of Mr. Soota when he was about to start Happiest Minds. The key fact here to note is the ability to judge & mention the next big thing in Indian IT in form of Cloud, Analytics & CRMs very early on -

Key risks to the investments-

Mr. Soota has been the pillar of strength for the company ever since it began. But what next? Happiest Minds does seem to have a strategy in place when it comes to succession. But how strong the strategy is only time will tell us.

Technology has always been disruptive in nature, especially when you earn maximum revenues from the latest technologies, like Happiest Minds does, leading to higher risks.

Thanks for reading! Share with someone who might be interested.

Disclaimers-

Personal & client investment/interest in the shares exist; this isn’t investment advice; DYOR (do your own research) is recommended; Investing & trading are subject to market risk; the Decision maker is responsible for any outcome