India's Own TikTok in Making

Can Meesho become the king of India's social commerce?

Hey there, it’s been ~9 months since I last posted here. The last few months have been overwhelming since I moved to Mumbai, and I’m grateful for all the great experiences this city has given me. I don’t plan to make this page as active as it used to be, but every once in a while, whenever I find some time, I’ll try to share my thoughts here.

I hope you enjoy reading today’s write-up. This is not investment advice in any form. For a better reading experience, you can read the full piece on the website here.

Rise of TikTok Shop

In November 2022, TikTok began testing its in-app commerce feature, TikTok Shop, in the United States. By then, the model had already proven successful in Southeast Asia, where it first launched in Indonesia in April 2021 before expanding across Thailand, Vietnam, Malaysia, Singapore, and the Philippines. TikTok Shop generated $4.4 Bn in GMV in 2022 alone. The formula was to combine entertainment with commerce to attract discovery-first, price-sensitive, mobile-native shoppers who were comfortable buying through content. At the time, TikTok already had more than 1.3 Bn active users globally.

What TikTok was trying to crack was something the big platforms had long pursued but never fully solved, which was the transition from social media to social commerce. Meta had experimented with Facebook Shops and Instagram Shopping. YouTube had tested shoppable videos, while Pinterest introduced product pins. Yet none had made content and commerce feel truly seamless. They remained, at their core, social platforms with shopping features layered on top. TikTok Shop was different. It was built so users could go from watching a creator to completing a purchase without ever leaving the video.

Amazon saw this as a threat. Within weeks, in December 2022, it launched Inspire, its own TikTok-style shopping feed built directly into the Amazon app. The company felt this new format could potentially reshape e-commerce in its largest market, especially with TikTok already boasting over 100 Mn users in the US who spent an average of 45 hours per month on the platform.

Fast forward to Feb ‘25, Amazon pulled the plug on Inspire as the feature had never found its footing. Creators abandoned it early. Amazon even tried to gain inorganic onboarding of creators in Aug’23, by inviting select influencers to submit videos, offering $12,500 for 500 videos or $25 for each qualifying video, but that experiment never worked out. Users never changed their behaviour, and Amazon’s app remained what it had always been: a search engine for things people already wanted to buy. ‘Inspire’ was a content layer dropped onto an intent-driven platform, and the two never reconciled.

Meanwhile, TikTok Shop continued on its path. It is now approaching half the size of eBay in the US, hosting more than 7 million domestic businesses, generating $15.8 Bn in sales for merchants, and is expected to surpass $23 Bn in GMV by 2026.

From the US, let’s return to Southeast Asia, where TikTok first found success with in-app social commerce, to understand how it is now challenging the region’s largest e-commerce (value-focused) player, Shopee.

The market here is increasingly consolidating into a tight duopoly. Shopee currently holds a 53% market share, while the combined TikTok Shop-Tokopedia entity has captured 35%. Meanwhile, Alibaba-owned Lazada has continued to lose ground, with its market share declining from 16% in 2023 to just 11% in 2025. While the broader e-commerce market is growing at 15-20%, TikTok Shop has been expanding at an explosive 90-100% year-on-year GMV growth rate, reaching $45.6 Bn in 2025. Short-form videos (reels) now drive nearly 60% of revenue in mature markets, while live commerce contributes 30-50% of GMV in regions like Indonesia.

Amazon is largely absent from this story, having never truly cracked Southeast Asia despite multiple attempts (read why).

Seeing live commerce explode in China, Shopee was actually one of the earliest e-commerce platforms globally to build the format natively into its app, launching Shopee Live in March 2019. While the company foresaw the rise of social commerce, and the feature now drives more than 25% of physical goods orders, Shopee remains, at its core, a value e-commerce platform with social features layered on top. That is precisely where TikTok Shop differs. It is built around social discovery first, which has helped it outgrow Shopee across the region. The share price of Sea Limited tells part of that story, having fallen by roughly half over the last 8 months.

Time to Talk about Meesho!

Before I get to the reason for writing today’s blog, let’s first set some context.

Social and live commerce have been buzzwords in India since the pandemic, but the model never truly took off. A number of startups attempted to build the category: SimSim was acquired by YouTube and later shut down, GlowRoad was acquired by Amazon, Bulbul went to Good Glamm Group, Shop101 was acquired by InMobi’s Glance, and Wooplr simply faded away. Even Meta shut down its live shopping feature in 2022 as it shifted its focus to Reels, a move that ultimately proved highly successful. Today, brands spend heavily on Instagram and WhatsApp to acquire users, before directing traffic to their own websites or fulfilling impulse-purchase demand through quick-commerce platforms.

Meanwhile, two of the world’s most successful social commerce platforms, TikTok Shop and Shopee, are effectively absent from India. TikTok was banned in 2020, while Shopee exited the market in 2022 (due to govt pressures), and neither appears likely to return anytime soon.

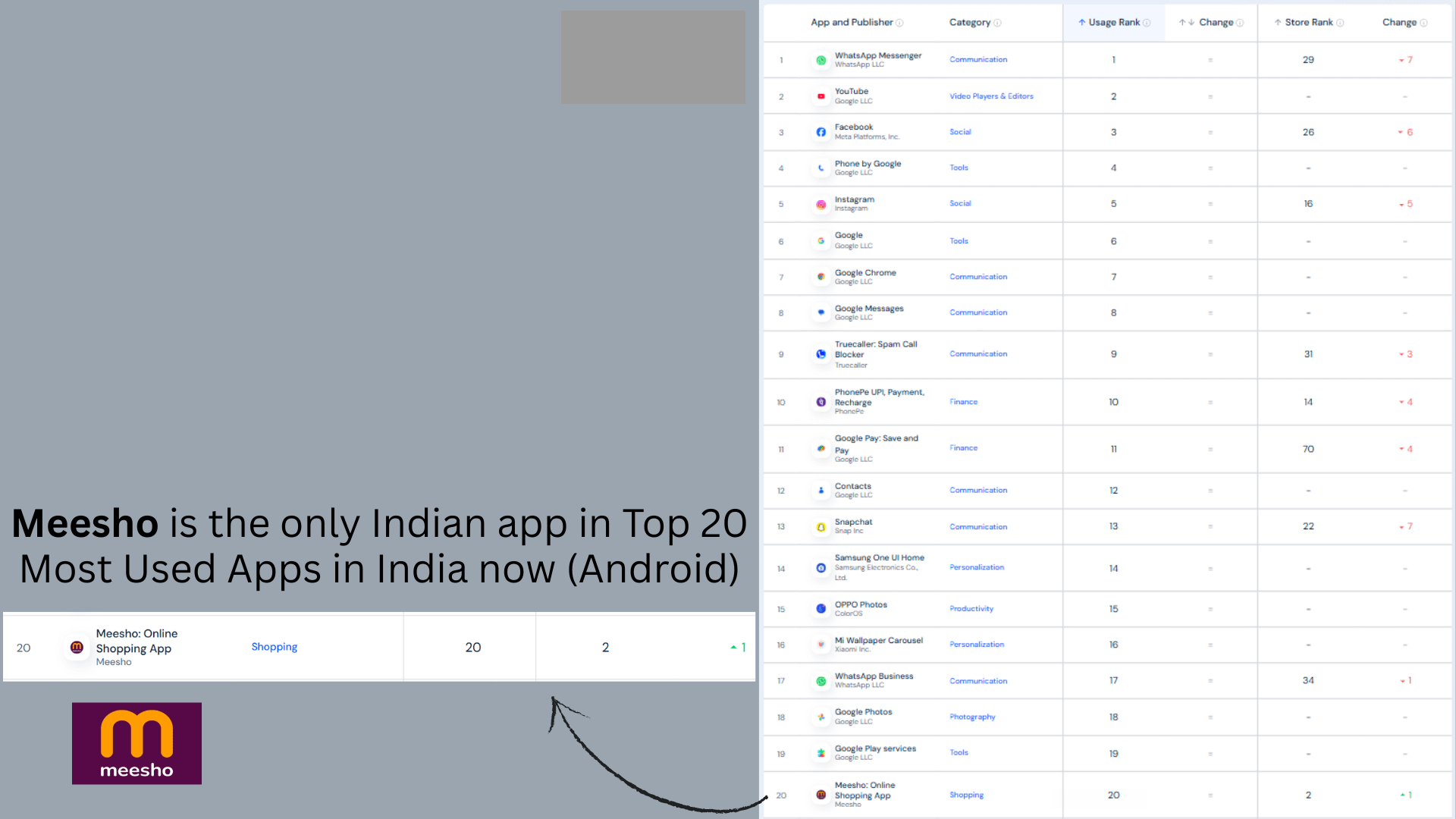

This is where Meesho stands out. It is India’s first major discovery-led marketplace, where users scroll and discover products rather than actively searching for them, much like browsing through a bazaar or supermarket in the offline world. Today, it is India’s largest e-commerce platform by order volume & user engagement, serving 263 Mn monthly active users who generate 153 Mn daily app opens and nearly 17 Bn product views every day. As of June 2026, Meesho is also the only Indian app among the country’s top 20 most-used apps and has remained India’s most downloaded shopping app since 2021.

Meesho originally began as a social commerce platform that enabled women, particularly homemakers, to resell products through WhatsApp and earn an income without holding inventory. Over time, as consumer behaviour evolved and online shopping became more mainstream, Meesho transformed from a reseller-led platform into a full-fledged marketplace focused on India’s value-conscious consumers.

But where is the Social angle today?

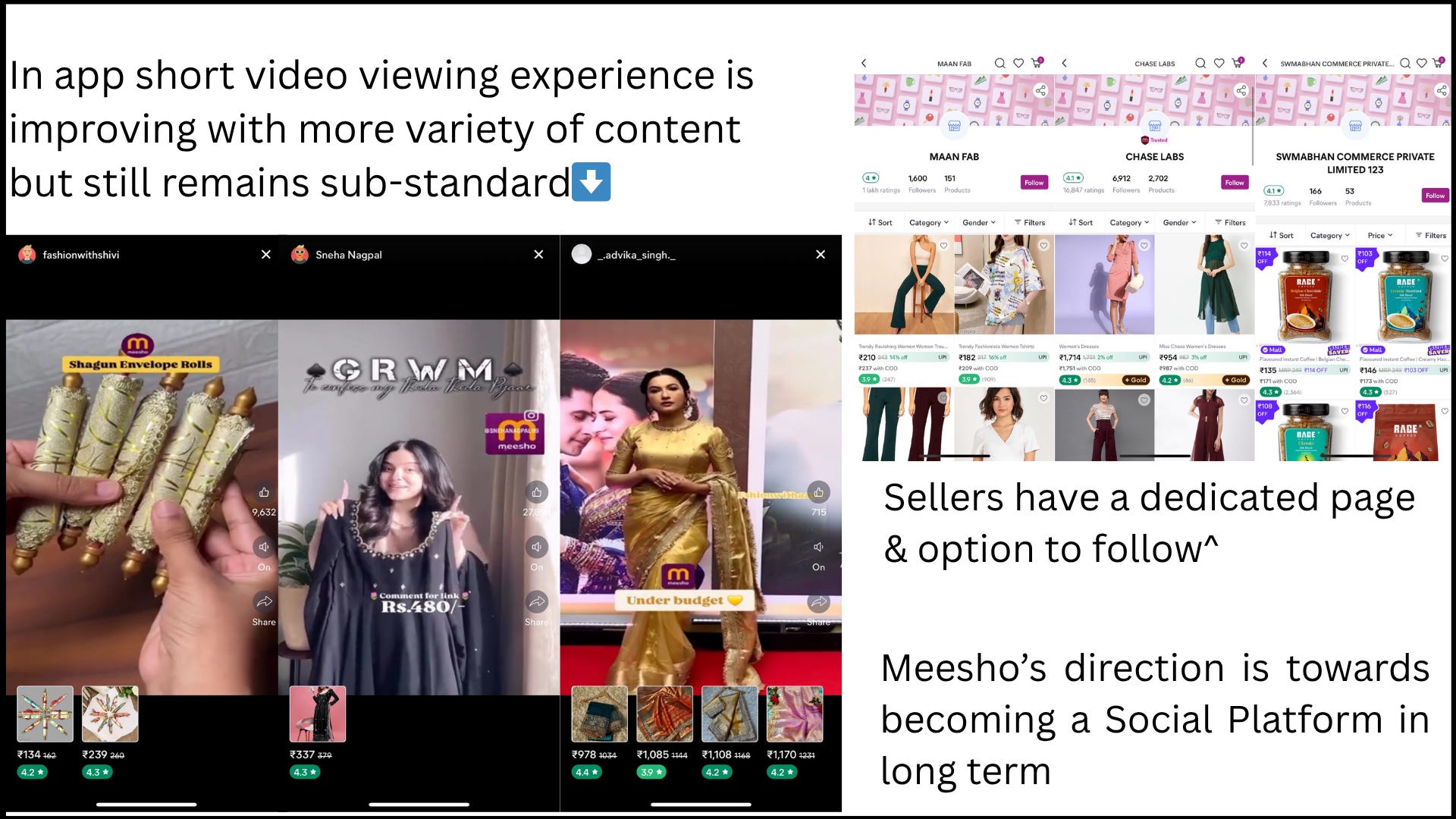

At its core, Meesho is powered by PRISM, an AI-driven recommendation engine that creates an endless, personalised product feed based on user behaviour. Alongside the traditional product grid sits ‘Video Finds’, where creators showcase products through short-form videos embedded directly into the shopping journey. These videos are increasingly being integrated into the main feed as well now, creating an experience that directionally looks similar to TikTok Shop’s discovery-led model.

The goal here is to improve discovery by allowing users to find products through creator-led demonstrations. Better product understanding builds trust, increases engagement + time spent on the platform, and ultimately translates into higher transaction frequency.

Amazon failed. Meesho likely to fail, too?

Inspire failed because Amazon was trying to convert users who arrived with purchase intent into the kind of impulse shoppers that power TikTok’s success. Meesho faces the opposite challenge. A large share of its user base, concentrated in Tier 2 & Tier 3 India, already browses without a specific purchase intent. These users are open to discovery, highly price-sensitive, and accustomed to consuming short-form video content on Instagram and YouTube. Meesho doesn’t need to change user behaviour; it simply needs to redirect it. The scrolling habit already exists, aided by its PRISM-powered recommendation feed.

But the bigger advantage lies elsewhere.

As mentioned earlier, Amazon paid creators up to $25 per qualifying video in 2023 because it never succeeded in building a self-sustaining creator ecosystem capable of producing high-quality content at scale. Without that supply of content, discovery commerce could never truly work.

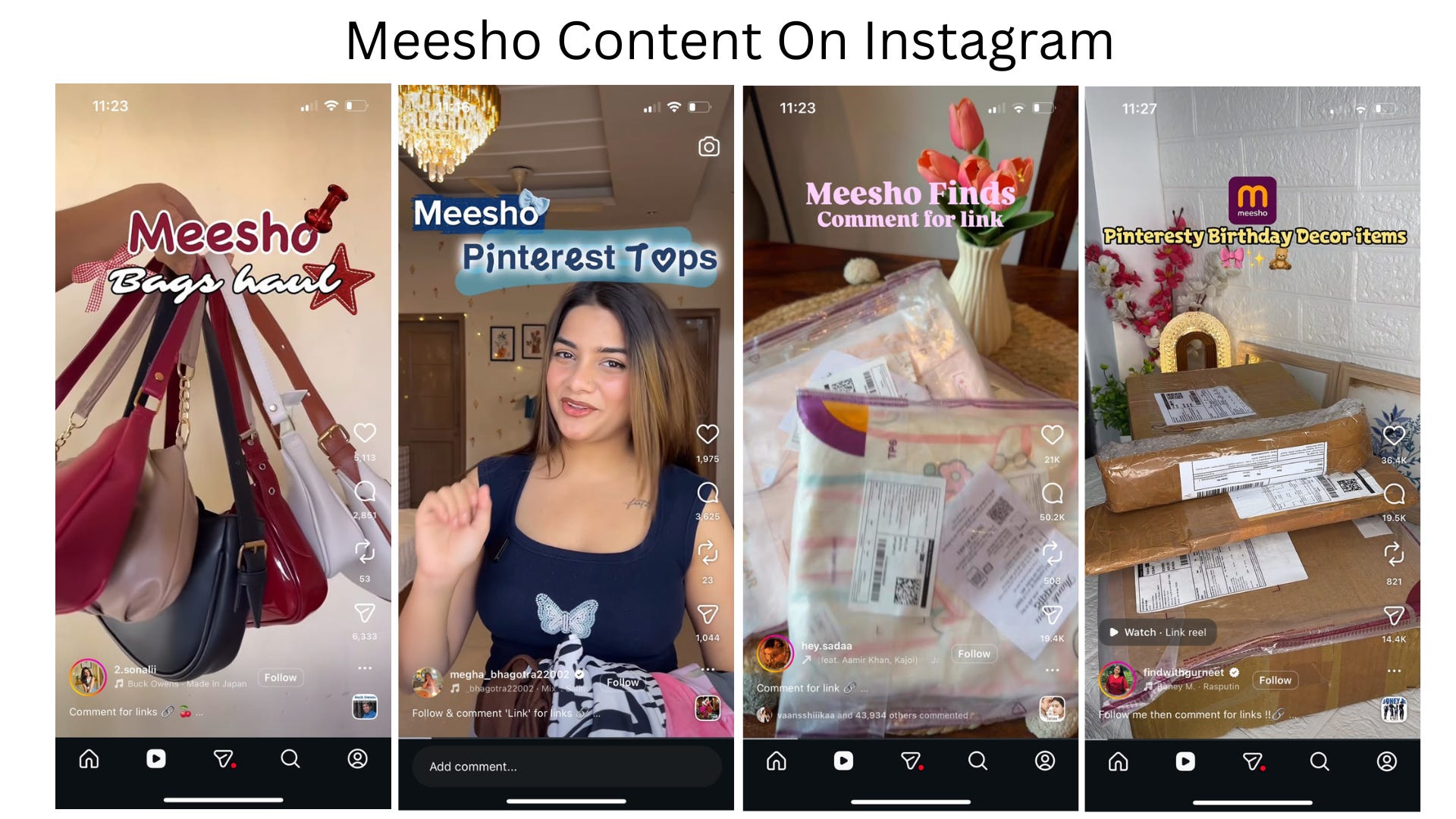

Meesho, on the other hand, already has a flywheel in motion. As of March 2026, roughly 14 lakh active, order-generating content pieces, primarily Instagram Reels promoting Meesho products, were contributing around 5% of the company’s NMV. A year earlier, that figure was estimated to be below 5 lakh, implying nearly 3x growth. The ecosystem spans a remarkably broad demographic: from a 65-year-old uncle creating reels to sell Meesho apparel, to a 20-year-old from a Tier 4 town reviewing home décor products and earning commissions on the sales they generate. Over the past few months, I’ve seen countless variations of this trend appear across my own Instagram feed.

In many ways, this resembles how Meesho grew during its first 5 years, when homemakers shared product photos across their WhatsApp networks to generate sales and earn commissions. The difference today is that Instagram has become the new WhatsApp.

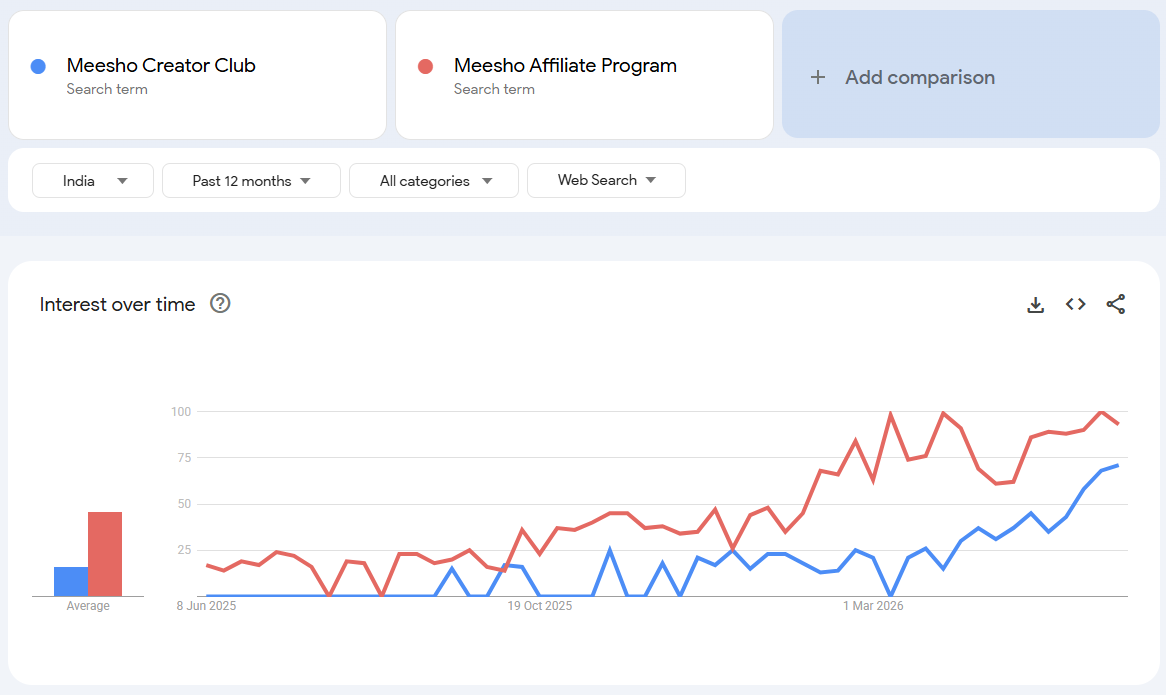

Meesho launched its affiliate program in May 2023 and significantly revamped it in Feb 2025 under the banner of ‘Meesho Creator Club’. A renewed push in Feb 2026 appears to have accelerated adoption, with the creator flywheel now beginning to take off. The company lowered entry barriers by removing minimum follower requirements while maintaining attractive commission rates (usually in the 10-15% range), enabling virtually anyone to participate. As a result, Meesho has onboarded thousands of creators who have collectively generated more than 4 million pieces of content.

Another way to gauge the growing interest among creators is through Google search trends. Searches related to Meesho’s creator registration page have risen over the past 12 months, with a noticeable acceleration since Feb 2026.

While affiliate marketing is not a new trend and has existed for years, what has changed over the past few years is the way content is consumed. The rise of short-form videos and reels has made creator-led commerce far more powerful, a shift that has made Meesho founder Vidit Aatrey increasingly bullish on content commerce, as reflected in his recent interviews.

One key challenge, however, remains unresolved: building a strong in-app social layer. Most creators today are not posting content on Meesho itself. Instead, they create content on platforms such as Instagram and YouTube, driving sales to Meesho through its affiliate program, where followers make purchases via shared links, and creators earn commissions on the resulting transactions.

In fact, before becoming an internet sensation at the 77th Cannes Film Festival in 2024, Nancy Tyagi was creating fashion content on Instagram, often featuring Meesho products and hauls. She began by stitching her own outfits and sharing them online, gradually building a following that eventually propelled her onto a global stage. Check out one of her Meesho reels from 2023 here.

While Meesho’s in-app short-video experience is improving, it still has a long way to go. After reviewing hundreds of videos on the platform, I noticed several basic issues: video quality remains inconsistent, many videos are not optimised for mobile viewing, products featured in videos are sometimes already out of stock, and prices shown in videos do not always match current listings, which sellers frequently update. These are foundational issues that ideally should not exist in the first place.

Overall, the viewing experience remains far from polished, although it is difficult to judge how Meesho’s core user base perceives it. One possible reason could be Meesho’s focus on maintaining a lightweight app, currently around 60 MB in size, which may require certain trade-offs. That said, I expect the company to continue investing in the experience over time. For Meesho to fully realise its content-commerce ambitions, the app will need to feel less like a traditional marketplace and more like a social platform, where creators can post their best content natively, build audiences, and engage followers directly rather than relying solely on external platforms such as Instagram.

Closing remarks

Whether Meesho ultimately succeeds in building India’s version of social commerce remains to be seen. The in-app experience is still far from perfect, and many of the key ingredients are only beginning to come together. But if social commerce is ever going to work in India, Meesho may be the closest thing we have to a serious contender.

Content commerce is only 5% of Meesho’s NMV as of Mar’26, but growing at 100%+ YoY. If the flywheel is real, this growth should accelerate & it should ideally cross 10% of NMV much faster than the market anticipates. Content-led commerce already drives more than 25% of orders at Shopee, while TikTok Shop is built almost entirely around that model. So why can’t the same be true for Meesho?

That’s it for today!

I hope you enjoyed reading the blog. Reply to this email to share your thoughts or drop in the comments section below. I read them all.

Disclaimers-

This isn’t investment advice but my personal thought process; DYOR (do your own research); Investing & trading are subject to market risk; the decision maker is responsible for any outcome. This blog is in no way related to my employer.

Very interesting take on how they are turning into a social company

Well written. Thanks for sharing your thoughts :)