Is India Overpriced?

The story of biggest single day downfall of my portfolio post-covid

On the 13th of March, 2024, my investment portfolio experienced a significant setback, plummeting by 4.2% in a single day, marking the sharpest decline since the onset of the COVID-19 pandemic. This prompted me to reflect on the potential causes behind this sudden downturn. Notably, my key holdings which I have covered multiple times before, such as DLF (available here), Tata Power (available here), and Zomato (available here) suffered substantial losses, erasing nearly 20% of the profits accumulated in the Financial Year 2024 in less than a week. At the broader market level, both the Nifty Smallcap 100 index and the Nifty Midcap 100 index witnessed substantial declines of 5.3% and 4.4%, respectively, marking their most significant single-day drops in almost two years.

While it's commonly understood that corrections within an up trending market tend to be temporary unless we're experiencing a structural downtrend or a full-blown 'Bear' market - which, I believe, is not the case here. In today’s blog, my aim is not to definitively assess whether markets are undervalued or overvalued by delving into P/E ratios. Instead, I'll explore potential reasons behind these sharp declines and discuss what might be driving them in the near future.

Note: If my emails end up in the ‘promotions’ tab, please move them to inbox so you don’t miss out. Don’t forget to subscribe and join 1K+ monthly readers!

Who thinks Indian markets are overpriced?

I intentionally selected the term "Overpriced" instead of "Overvalued" in the headline of this blog, as there exists a significant distinction between the two. Pricing occurs when we attempt to compare assets of similar nature and value our asset based on how other assets are valued by the market, whereas valuation encompasses many more aspects beyond simply pricing based on ratios. Here is a 2-minute video by Prof. Damodaran explaining the difference between the two concepts:

But why overpriced?

A few days ago, Whirlpool Corp, the largest appliances company in the USA, sold 30.4 million shares of its Indian subsidiary, Whirlpool India, representing a 24% stake in Whirlpool of India, through the open market for $468 million. This move was aimed at reducing the debt on its books. As a result of the sale, the parent company's ownership in its Indian unit decreased from 75% to 51%. While this transaction may seem normal as they still hold majority stake, what caught my attention was the statement made by the Global CEO, Marc Bitzer, during his interview on CNBC. He highlighted that the shares of Whirlpool India were trading at approximately 50 times the P/E ratio, whereas the parent company's shares listed in the US were trading at a much lower P/E ratio of around 12 times. Bitzer referred to this difference as 'arbitrage'. To watch his full interview, click on the link below.

Whirlpool is not the only company capitalizing on this fact, rather there are many more promoters doing the same. Interestingly, just a month ago when rumors surfaced about Hyundai India's potential listing, the share price of its parent company, Hyundai Motor Co, listed on the Korean exchange, surged over 30% in just 10 days. The primary reason for this surge? The anticipation of an Indian listing. Auto stocks, catering to the growing demand for cars in India and listed on Indian exchanges, tend to command premium valuations. For instance, Hyundai's parent company trades at a price-to-book ratio of 0.69 times in Seoul. In comparison, Indian automakers like Tata Motors trade at 6.48 times and Maruti Suzuki at 4.96 times (as reported in an article published a month ago). Interestingly, Hyundai is contemplating a valuation of $30 billion for its Indian unit IPO, according to sources. This valuation exceeds 65% of its Korea-listed parent's market capitalization, which stands at $46 billion in Seoul, despite the fact that only 15% of their total cars sold worldwide are sold in India. Sources said Hyundai wants to cash in on this growth and also tackle the "Korea discount", a term analysts use to refer to the typically lower valuations for South Korean companies compared to global peers because of lower dividend pay outs, the dominance of opaque conglomerates and geopolitical risks involving North Korea.

Returning to March 13, 2024, the day of the significant market downturn, the second major headline after news of the crash was the stake sale by British American Tobacco, the controversial parent company of India's largest tobacco firm, ITC.

They sold a 3.5% stake in ITC, reducing its total holding to approximately 25.5%. Market veteran Sunil Singhania, founder of Abakkus Asset Manager LLP, tweeted on how the rich pricing multiples of Indian subsidiaries or associate companies, such as ITC in this case, are prompting foreign entities to cash in on them in an attempt to improve their capital allocation strategies.

Foreigners don’t love India?

Since the onset of COVID-19 in 2020, the ownership percentage of foreign institutional investors (FIIs) has been decreasing. However, a declining percentage of FII shares in Nifty 50 stocks doesn't necessarily imply selling pressure from them alone. This trend is also influenced by the influx of excess funds into the markets from mutual funds and retail investors, who are gradually gaining a larger share of ownership in our Nifty index, along multiple other reasons.

In fact, share of foreign promoters ownership in Nifty 50 index has been steadily declining from 7.3% in December 2020 to 6.5% in September 2023. You can find all this data in NSE Pulse.

So, 13 March 2024 was another day where FIIs were big sellers in Indian market. Despite positive global cues, after adjusting for ITC block deal, FIIs actually sold Rs 15,580 Crores worth of shares in Indian markets on a single day. Along that, they have been continuously selling in January and February too, with total selling of Rs 15,963 Cr and Rs 35,977 Cr respectively.

Now moving on to our 2nd culprit.

Fear is in the Air

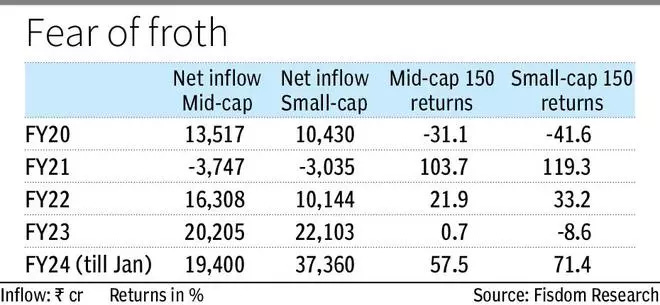

Mid and small-cap mutual funds in India have been experiencing unprecedented inflows, reaching levels never seen before since the onset of COVID-19. Retail investors are flocking to these funds as if there's no tomorrow. For instance, net inflows into small-cap mutual funds in FY24 are expected to be four times the amount received in FY20, just before the pandemic hit. As India's affinity for the equity asset class deepens, investors are increasingly drawn to mid and small-cap funds in pursuit of higher returns.

This surge in inflows has presented a dilemma for many fund managers. They find themselves grappling with how to deploy such substantial amounts of lump sum investments they have been receiving since last year. The challenge lies in finding investment opportunities that meet their valuation criteria, as suitable options are limited in the current market landscape.

A slew of events in the last 2-3 weeks have actually accelerated fears amongst many fund managers and investors about the rise of market ex-large caps.

On February 28th, the Association of Mutual Funds in India (AMFI), an industry body for asset managers, urged its members to moderate inflows into small and mid-cap funds. The aim was to safeguard investors from potential risks associated with large outflows, as robust inflows had raised concerns about a potential market crash.

On 11th March, the SEBI chief came out with a warning that there are pockets of froth in the market. She said, “It may not be appropriate to allow that froth to keep building…..(else) there is a risk of bubble in stock market”

On 12th March, ICICI Prudential Mutual Fund became the fifth mutual fund to temporarily suspend fresh subscriptions through lump-sum investments and switches into its small-cap and mid-cap funds

On March 13th, when the markets opened, selling pressure from foreign investors combined with fear among domestic funds and investors created a double whammy effect for the markets. This resulted in a lack of confidence among buyers to step in and buy the dip, leading to a continuous free fall in the market throughout the day. The absence of significant buying activity exacerbated the downward trend, causing a notable decline in market indices.

What next?

Though its hard to predict where the markets are headed from here and markets generally tend to prove you wrong often when you attempt to do that, there are certainly 2 key take aways from the incidents mentioned in this blog:

We are fortunate to have proactive and effective regulators in India, whether it's the RBI or SEBI. The adage "Better Safe than Sorry" rings true, and these regulators have consistently followed this principle. The new measures being implemented by SEBI, such as stress tests for mutual funds to protect investor interests, can serve as a stepping stone towards building a resilient financial system that supports long-term growth. These proactive measures demonstrate a commitment to safeguarding investor interests and ensuring the stability of the financial markets.

Mutual funds have played a crucial role in raising awareness among Indians about the equity asset class and the benefits of long-term investing. The decision of mutual funds to halt inflows in lump sum amounts is commendable, as it demonstrates a commitment to the long-term health of the industry. While this may result in reduced business in the near term, it is ultimately a positive move for the industry as a whole. I don’t know if its right to halt inflows into their fund, but by prioritizing investor interests over short-term gains when they feel froth in certain segments of market, mutual funds are contributing to the creation of a more sustainable and resilient investment ecosystem.

In the end, I personally feel if this dip continues further, it can be a good time to invest in the stocks I am a believer in. As India’s long term story remain intact, the fall of 13th March 2024 was surely treacherous but it was not nerve wracking. If you enjoyed reading today’s blog, consider sharing it with your friends and help me grow.

I'm grateful to Krishang Baldi for assisting me with research of this blog. Our next piece, focusing on Blinkit/Zomato, will be released in the coming weeks (Update: Available here). Subscribe and stay tuned!

Wondering how you can support us?

If you find our content valuable & are willing to support, show some love here⬇️

Thanks for reading the Finding Outperformers. This post is public so feel free to share it!

Disclaimers-

We are not SEBI registered advisors; personal investment/interest in the shares exists for the company mentioned above; this isn’t investment advice but our personal thought process; DYOR (do your own research) is recommended; Investing & trading are subject to market risk; the Decision maker is responsible for any outcome.

| A guest post by

|