Is the Elephant back in the ring?

Part 2: Discussing how HDFC Bank is trying best to get out of the mess

Update: This blog was written before the Q4 FY24 results which came out on 20th April. The results were on the expected lines. NIMs expanded by 4 basis points and the management did confirm in the Q4 results concall that they have intentionally taken the call to reduce their wholesale book due to low yield - exactly what we discussed in the blog below, happy reading the original version below!

In my recent note (“Part 1 - Did the elephant fall while dancing?”) following the Q3 FY2024 results, I discussed HDFC Bank's sudden dive into a messy situation. With liquidity drying up in the banking system and RBI softly hinting at banks to maintain a healthy 'Credit to Deposit' (CD) ratio, while banking deposit growth has been sluggish since the onset of Covid, the outlook appeared grim. We concluded that the bank would need to swiftly restore the CD ratio to pre-merger levels, implying either a significant slowdown in loan growth or raising interest rates on customer deposits to accelerate growth on that front. This also implied that the trajectory of margins continues to remain uncertain.

What unfolded was entirely expected. HDFC Bank not only raised customer deposit rates on select tenures of their fixed deposits since the results but also significantly lowered their loan growth. Emerging trends suggest that, to protect margins, they are planning to significantly change their loan book mix in the quarters to come. Now, let's get started!

Note: If my emails end up in the ‘promotions’ tab, please move them to inbox so you don’t miss out. Don’t forget to subscribe and join 1K+ monthly readers!

Deposit competition is still ON!

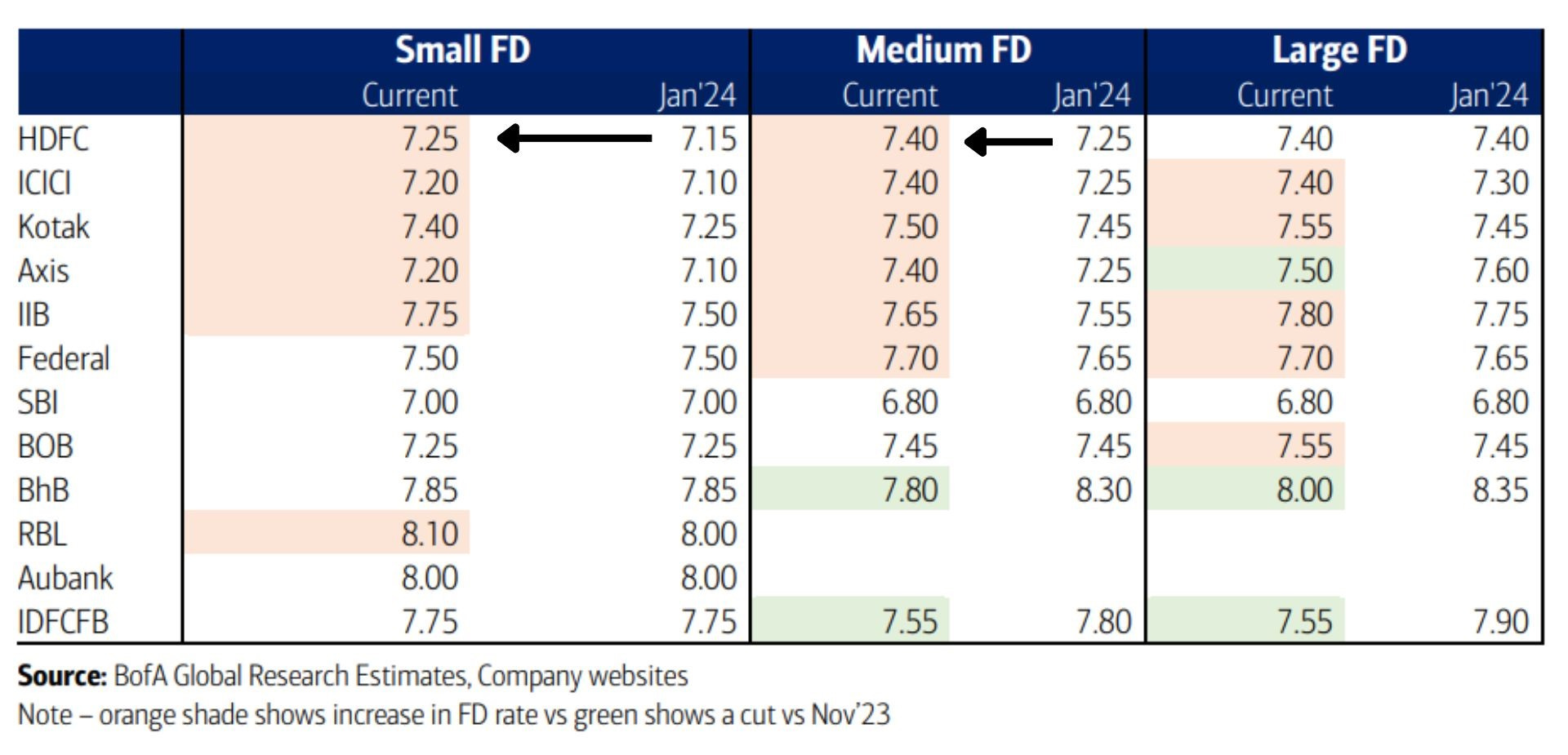

The crucial point of discussion here is that the revision of Fixed Deposits (FD) rates is still ongoing, even a year after the last repo rate hike by the RBI. In an ideal scenario, it usually takes a few quarters for FD rates to adjust to rate changes made by the central bank. However, this hasn't been the case in India. Banks, struggling to gain customer deposits, have had to raise their rates yet again in recent months.

Here's a summary of how various banks have increased their rates since January 2024 and how HDFC's FD rates have risen alongside others:

As indicated in the table from BofA report, not only HDFC Bank but all the Big 4 banks have increased their peak FD rates for both retail and bulk FD by up to 25 bps, now offering 7.2-7.4% for retail and 7.4-7.55% for bulk FD. Among these banks, Kotak Mahindra Bank continues to offer the highest rate, 10-20 bps higher than its peers. Additionally, HDFC has recently introduced a special FD with a 7.25% rate for a 540-day tenure, while ICICI Bank has introduced a special scheme for senior citizens with a rate 5 bps higher at 7.75%.

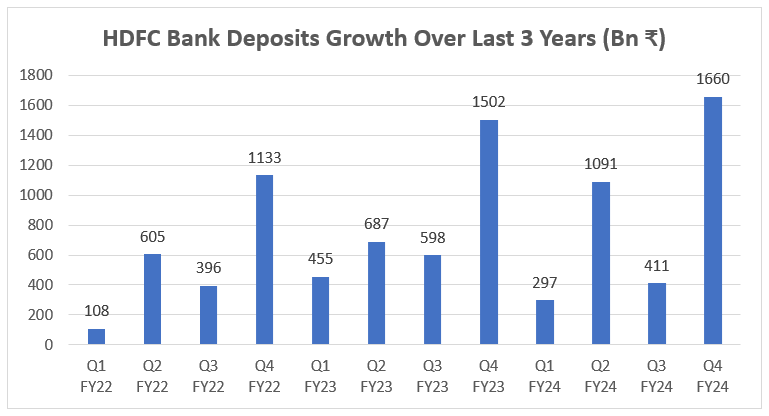

On the deposits front, in the just released quarterly update for Q4 FY24, HDFC Bank reported a significant gain of Rs 1660 billion in deposits. For comparison, the total deposits gathered by IDFC First Bank till date are nearly Rs 1760 billion. This implies that HDFC Bank added another IDFC First Bank (in terms of deposits) in just one quarter :)

One of the key disappointments of Q3 FY24 from HDFC's results was the slower-than-expected deposit growth, where it raised just Rs 411 billion, coupled with slower-than-expected net interest margins. Putting that in context, it seems like HDFC was able to raise an amazing amount in the last three months of FY 2024, especially at a time when liquidity was tight in the banking system. However, before I praise HDFC Bank more for this achievement, let me zoom out a bit and examine the trend of raising customer deposits for the bank over the last three years:

Interestingly, there's some seasonality involved as HDFC Bank tends to gain a significant chunk of its total deposits raised in the fiscal year specifically in the last quarter, and this year was no exception. In FY22, 51% of the whole year's deposits were raised in Q4, while in FY23, this figure was at 46%. Similarly, in the just completed fiscal year 2024, 48% of the whole year's deposits were raised in the last quarter. This year also benefited from the added reach and network effect of HDFC Ltd, which merged with HDFC Bank on July 1, 2023.

In summary, HDFC's ability to capture such a large portion of the deposit system is commendable, especially given the tougher liquidity conditions this time around. However, this achievement wasn't entirely unexpected, considering HDFC Bank's track record. Therefore, while the performance is noteworthy, it may not lead to an immediate re-rating in its stock price, as the bank has demonstrated its ability to achieve similar results in the past as well.

No more Loan Melas?

HDFC Bank's loan growth is now significantly slowing down as expected. This strategy enables the bank to bring its 'Credit to Deposit' ratio below 100% faster, eventually aiming towards around 80%, in line with RBI's medium to long-term expectations for all banks. In the January-March period, their loan book grew by just 1.6% quarter-on-quarter (QoQ), compared to a 7.5% growth in deposits on a QoQ basis. This marks a significant slowdown for a bank that has historically grown its loan book at a rate of ~ 18% to 20% over the last decade.

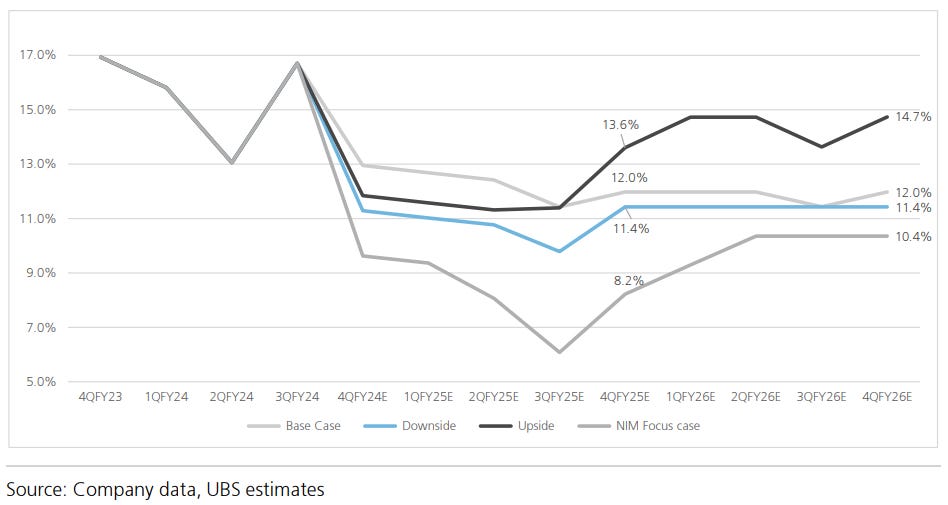

Below are the expectations from the UBS research report regarding how HDFC Bank's loan book might grow in the coming quarters and years. Similarly, most research houses are now anticipating a loan growth of 11-12% for HDFC Bank in the next two years, namely FY25 and FY26:

That said, one thing which is emerging as a strategically planned move of HDFC Bank is to change its loan book mix in order to boost its NIMs faster. Let me explain - HDFC categorizes its loan book in 3 major segments mentioned below:

Retail loans include the loans given to Auto Loans, Credit and Debit cards, Personal Loans, Mortgages, etc.

Commercial & Rural banking loans catering to the needs of the Micro, Small and Medium Enterprises (MSME), emerging corporates, commercial agriculture, etc.

Corporate and Wholesale banking loans involving corporates, institutional customers, government agencies, local governments, etc.

When its comes to margins, Retail + Commercial & Rural banking are more profitable lending spaces along with higher risks. When the economy is doing well, these segments tend you boost a bank’s return ratios (ROA and ROE) to much higher levels, but if the economy goes down, these segments default the first. Where as, the Corporate & Wholesale book is relatively low risk, low reward segments of lending business because of the customer set your are dealing with which are better governed and tend to have deeper pockets. For example, about 88% HDFC’s Wholesale book is rated ‘A’ and above which displays the safety of lending to such corporates.

The reason I brought this aspect up is because HDFC Bank seems to looking to de-prioritizing this low margin segment lending business in order to improve its margins (NIMs) going ahead. Here is how the 3 segments grew in January to March 2024 period:

Retail loans grew +3.7% on Q-o-Q basis

Commercial & Rural banking loans grew +4.2% on Q-o-Q basis

Corporate and Wholesale banking loans grew -2.2% on Q-o-Q basis

A degrowth in Corporate/Wholesale book along faster acceleration of high margin business segments helps HDFC boost its NIMs towards the magical mark of 4% faster. Though the overall growth rate of loans to corporates/wholesale loans has been slow at overall banking level as well, this segment was growing 1.9% Q-o-Q for HDFC Bank in Q3 FY24, and did grow a healthy 4.4% Q-o-Q last year in Q4 of FY23. Unless it's a one-time change resulting from some reclassification of loan accounts, which the management would likely clarify post-results, or something of a temporary nature, it does seem like a strategically taken decision by HDFC Bank. This implies that the bank is actively repositioning its loan book mix for profitability and to achieve its desired NIMs targets.

To Summarize:

HDFC Bank is trying to kill 2 birds with one stone. On one side they have to grow their deposits at much faster pace than the banking system's growth, and simultaneously have to boost their margins in order to meet the expectations of the street on profitability front. And the latest quarterly updates hints at exactly that which elated the street post the update.

Their deposits are growing strongly at 7.5% QoQ, and they are increasing the high-margin portion of their loan book at the expense of the low-margin loan book. This strategic move is expected to support NIM expansion in the coming quarters and years.

Seems like HDFC Bank is trying to get back in the circus ring, but will it also start to dance again? Thanks for reading till here, share the blog if you find it useful. Find me on LinkedIn here.

Wondering how you can support us?

If you find our content valuable & are willing to support, show some love here⬇️

Consider reading my previous blog on HDFC Bank (Part 1) below:

Did the elephant fall while dancing?

Recently India’s largest bank by market cap, HDFC Bank, lost INR 1.3 lakh crores in market cap in just 1 week of announcing its Dec ’23 results.

Disclaimers- We are not SEBI registered advisors; personal investment/interest in the shares exists for the company mentioned above; this isn’t investment advice but our personal thought process; DYOR (do your own research) is recommended; Investing & trading are subject to market risk; the Decision maker is responsible for any outcome.