Slowing NII growth, what next?

Read how different banks are placed on 'Fee Income' front

Recap

In August of this year, we released our blog titled "Is Bank Nifty Losing Its Charm?". In this blog, we delved into the challenges that banks in India are currently grappling with, particularly the intense compression of margins, which adversely affects their Net Interest Income (NII) growth rate. Since August, Bank Nifty has underperformed the Nifty 50 index till the date of publishing this blog.

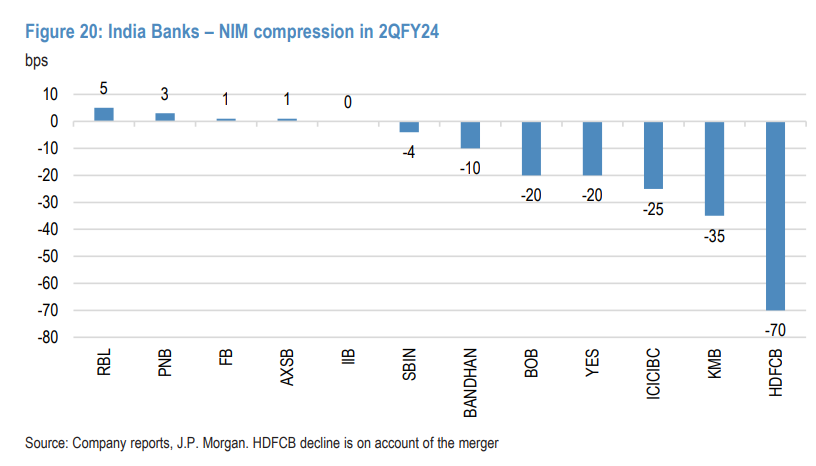

The margins of India's largest bank, SBI, compressed by 27 basis points in Q1 FY24 alone. The trend continued into Q2 FY24, with many other banks experiencing sustained pressure on their margins. A case in point is depicted in the graph from JP Morgan, illustrating how major banks in India, such as Kotak, ICICI, BoB, and SBI, have consistently faced challenges due to the rising cost of deposits:

Due to the record margin expansion that followed COVID period, the bank's top line increased by over 25% across all banks, including PSUs, until the early months of this year. However, this trend is currently reversing. The effect of this margin compression on bank topline growth is shown below, which analysts generally agree has peaked since, in addition to compressing NIMs, the system's loan growth also appears to have stabilized:

Note: If my emails end up in the ‘promotions’ tab, please move them to inbox so you don’t miss out. Don’t forget to subscribe and join 500+ readers!

RBI delivers a Shocker!

In November 2023, the Reserve Bank of India (RBI) took a proactive step by increasing the risk weights for both banks and non-bank financial companies (NBFCs) by 25 percentage points, bringing it to 125% specifically for retail loans. This change signifies the amount of capital that banks are required to set aside for every loan. In simpler terms, banks now need to maintain a higher capital buffer for personal loans provided to customers and for retail loans extended to NBFCs. While this excess capital buffer enhances the overall safety of the banking system, it has a detrimental effect on the profitability, as well as the return on equity/asset for banks.

The move was prompted by a substantial increase in unsecured personal loans, which saw a 23% rise compared to the previous year as of September 22, 2023. Additionally, outstanding amounts on credit cards surged by nearly 30%, surpassing the overall banking credit growth of ~15% during the same period. The RBI had issued verbal warnings to banks on multiple occasions, urging caution, especially with certain categories such as small-ticket size personal loans experiencing rapid and potentially unsustainable growth.

Recent data from credit bureau Transunion CIBIL, released earlier this month, revealed that delinquencies, defined as loans overdue by more than 90 days, were at 0.84% for all personal loans. However, for loans below ₹50,000, delinquencies were significantly higher at 5.4%. In response to these concerning trends, the RBI took a measured approach to steer the banking system toward a safer future. This regulatory action is expected to impact the overall credit growth rate for banks, particularly those with a focus on retail lending and NBFCs. If you are interested in a more in-depth explanation, please feel free to delve further into the details:

What can drive higher profitability for banks in future?

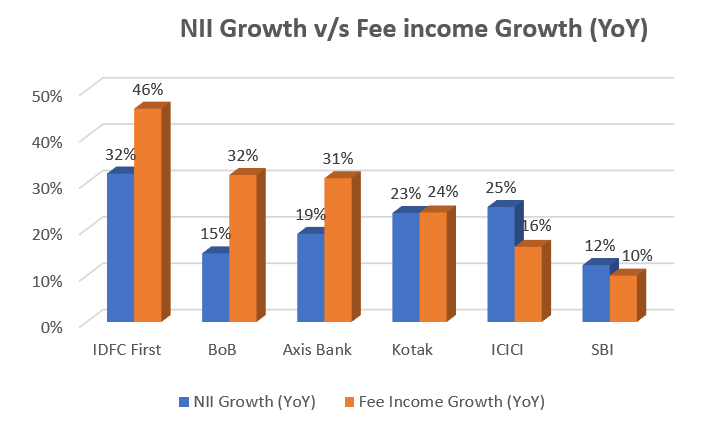

After grasping the adverse impact of net interest margin compression and the recent RBI guidelines on the return on equity of banks, as they influence the primary income source—net interest income (NII), we now shift our focus to the second-largest income source: Fee Income. Presented below is a graph depicting the latest growth numbers for Q2 FY24 among the major banks (excluding HDFC Bank, given the significant impact of the merger on core numbers):

We shall now touch upon each of the all these banks talking about how their core banking fee income is doing and what’s driving it:

Kotak Mahindra Bank & ICICI Bank

These two major private banks hold the 4th and 5th positions among the six banks selected for our analysis, and their fee income has either matched or fallen below the net interest income (NII) growth rate. For these banks, fee income constitutes approximately 25% to 30% of their core net interest income from banking. However, it's crucial to note that these banks operate diverse businesses, including asset management, broking, investment management, investment banking, advisory fees, and more. For instance, Kotak Securities and ICICI Securities are their entities in the share broking, while Kotak AMC and ICICI AMC rank among the largest asset management companies (AMCs) in India.

Considering this broader perspective, we can affirm that although the core banking fee income may not show significant growth, these banks possess a broader scope and the ability to enhance their fee income through various revenue streams. In fact, the consolidated 'fee income' for ICICI Bank surged by an impressive 68% YoY in the latest quarter, taking into account the impact of all its subsidiaries.

In the case of ICICI Bank, a strong emphasis on digitization and cards for both retail and business segments has yielded positive results. The bank has successfully activated over one crore iMobile Pay accounts by non-ICICI Bank account holders to date, significantly contributing to the other income, particularly the fee-based income of the bank. Additionally, ICICI Bank commands a substantial market share of about 30% by value in electronic toll collections through FASTag in Q2-2024, experiencing a 15.4% YoY growth in fee collections.

On the other hand, as per Kotak Bank's FY23 annual report, the rise in fee income is primarily attributed to an increase in commission, exchange, and brokerage income. This is mainly driven by higher service charges on loans, direct banking fees and charges, credit card fees, third-party distribution income, and referral fees.

State Bank of India & Bank of Baroda

Before delving into the discussion on public sector banks, it's essential to highlight that 'fee income' for them constitutes less than 20% of the net interest income, a notably lower proportion compared to the ~30% earned by the aforementioned private banks. Additionally, there exists a significant disparity in the growth trajectories of fee income for the two major public sector banks.

Bank of Baroda (BoB) stands out with an impressive 31% growth in fee income, surpassing many of the private sector banks mentioned earlier, albeit starting from a relatively lower base. This growth outpaces State Bank of India's (SBI) modest 10% growth rate, which is the lowest in the group. SBI's fee income growth is primarily driven by a notable increase in 'Loan processing fees,' which witnessed an 18% year-on-year growth.

For BoB, over 50% of the fee income is derived from commission and brokerage earned through banking operations. The management expresses confidence that the growth in fee income and non-interest income will be substantial in the coming quarters as they focus on optimizing Net Interest Margin (NIM) in response to the evolving scenarios in the banking landscape.

Bank of Baroda (BoB) has strategically initiated a move to enhance its fee-based income through a program known as Fees and Flows (F&F). This initiative is coupled with a significant focus on expanding the adoption of Cash Management Services (CMS) to attract a broader customer base. The overarching goal is to stimulate more cash flows within the system, enabling the bank to tailor products to meet specific customer needs and thereby drive fee-based income.

Traditionally, CMS was predominantly a corporate product. However, BoB is now extending its reach to mid-corporate and MSME (Micro, Small, and Medium Enterprises) sectors as well. This strategic shift has yielded positive results, as evidenced by the substantial increase in the number of customers onboarded by the bank in the last six months of FY24. Remarkably, this figure is nearly equal to the number of customers onboarded in an entire year over the preceding several years. This surge in customer acquisition highlights the effectiveness of BoB's approach to diversify its CMS offerings and target a broader market, resulting in a significant uptick in fee-based income.

Axis Bank

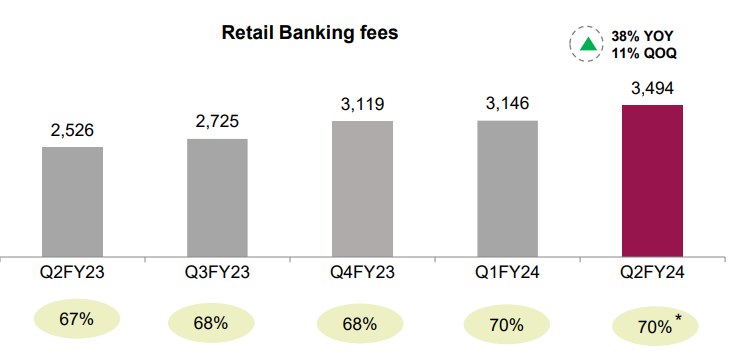

Axis Bank has not only positioned itself as one of the fastest-growing banks, exhibiting an impressive 31% YoY growth in fee income, but it also stands out with this income accounting for a substantial 40% of its Net Interest Income, the highest proportion among its peers. This remarkable performance can be attributed to Axis Bank's strategic acquisition of Citibank's India business. Through this acquisition, the bank gained access to a large and affluent customer base, along with a diverse array of fee-oriented and profitable business segments. These segments encompass a high-quality cards portfolio, an affluent wealth management clientele, and meaningful retail granular deposits. This strategic move has significantly contributed to Axis Bank's robust financial performance and strengthened its market position. ‘Retail Banking’ fees now comprises 70% of total fees earned by the banks and has grown 38% on YoY basis:

A significant shift in profitability over the past four years for Axis Bank has been the transformation of its fee profile. Previously dominated by credit-linked fees, the bank has strategically pivoted towards a more sustainable transaction banking fee franchise. This shift has been pivotal in their success, as evidenced by winning substantial mandates across various domains, including current accounts, cash management, trade finance, sector-specific smart solutions, and government businesses. These victories, driven by technology-led offerings, have resulted in transaction banking, forex, and trade-related fees comprising over 75% of their 'Wholesale Banking' fees, contributing to approximately 30% of the total fee income in FY23. On the 'Retail fee' side, which constitutes 70% of the total fee income, the third-party distribution business has played a significant role in recent growth. This can be attributed to strong partnerships, strategic product launches, extensive distribution networks, and digital initiatives, leading to a remarkable 62% year-on-year increase.

Axis Bank's standout performer in the retail fee category remains its robust credit card business, contributing around 30% to the total fee income. This segment continues to grow at a healthy and sustainable pace, underscoring the bank's success in diversifying and optimizing its fee-based income streams.

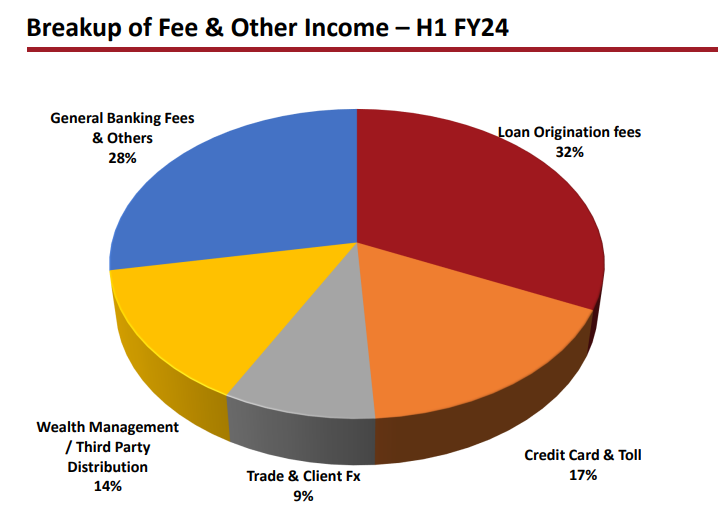

IDFC First Bank

Concluding the analysis, IDFC First Bank stands out as an emerging and robust contender in the retail banking space, showcasing the fastest pace of fee income growth in recent quarters. While the proportion of fee income to Net Interest Income (NII) is ~30%, which is lower when compared to Axis bank, it is notably higher than the fee-charging practices of public sector banks. This strategic positioning allows IDFC First Bank to demonstrate a competitive edge in generating fee-based income.

Given this distinction, the bank's management has provided forward-looking guidance, expressing confidence that fee income will continue to grow at double the rate of the NII growth rate in the quarters to come. This strategic forecast underscores IDFC First Bank's commitment to further expanding and diversifying its fee-based revenue streams, signaling its strong potential and trajectory in the dynamic and evolving landscape of retail banking.

The bank has been growing its branches at a high rate of ~20% YoY over past many quarters which is opening possibilities for the banks to strengthen its retail model. In last few years, the bank launched many new products which are in the early stage of their lifecycle and have the potential to grow significantly going forward. Certain fee generators like wealth management products and distribution from third-party have increased by over 80% (Y-o-Y) in past few quarters on a low base.

On a separate side, CEO V. Vaidyanathan recently did mention this statement in one of their investor con-calls which caught my attention,“We are not exactly doing a great job in getting fee income from customers as you know most of our services are free there and even for our cross sell, you may not have got many calls from the Bank to sell you the product because we keep it very little tone down because we don't want to disturb customers but net-net there's a fee income, there's a big opportunity for us on the fee income side to grow it.” Here, he is referring to the act of waving off the fees on 25 commonly used banking services in saving accounts like the fee on the number of cash transactions, IMPS transaction cost, passbook charges, etc. which they did in the 2nd half of 2022. Read more about this initiative below:

That’s it for this blog! We shall be keeping a close watch quarter after quarter and bring such analysis around Indian banks to our subscribers. Onto our search for next outperformer!

See ya!

Disclaimers-

We are not SEBI registered advisors; personal investment/interest in the shares exists for the company mentioned above; this isn’t investment advice but our personal thought process; DYOR (do your own research) is recommended; Investing & trading are subject to market risk; the Decision maker is responsible for any outcome.

| A guest post by

|

| A guest post by

|