The Broken Indian Healthcare System

What issues does India face today & how is PB Fintech trying to solve them?

Affordable healthcare for middle class India is a myth. I recently met one of my mentors after 6 years, who had suffered from Covid-19 during the 2nd wave in 2021 and had to be admitted to a hospital for about 80 days due to his lungs and heart collapsing within a week of getting Covid. Result? While his courage helped him survive (and now even thrive), it came at a financial cost of ₹3 crores as he didn’t have insurance, wiping out all the savings (financial assets) his family had accumulated so far and leaving them vulnerable to any future financial uncertainty.

Not many in the Indian middle class are lucky enough like him - not just to fully recover but also to maintain their hard assets. With partial or no insurance protection, the impact is often full-blown.

In case you are new to this website, join over 4,200 readers by subscribing for free to receive new posts directly in your inbox!

Over 60% of healthcare expenses in India are paid out-of-pocket - one of the highest rates in the world. Even for India’s largest hospital chain Apollo Hospitals, 40% of revenue comes from patients who have no option but to pay out-of-pocket. Private hospitals have now become the default option due to the poor state of public healthcare. Soaring consultation fees, expensive diagnostics, and skyrocketing insurance premiums have made many medical care services a significant financial burden.

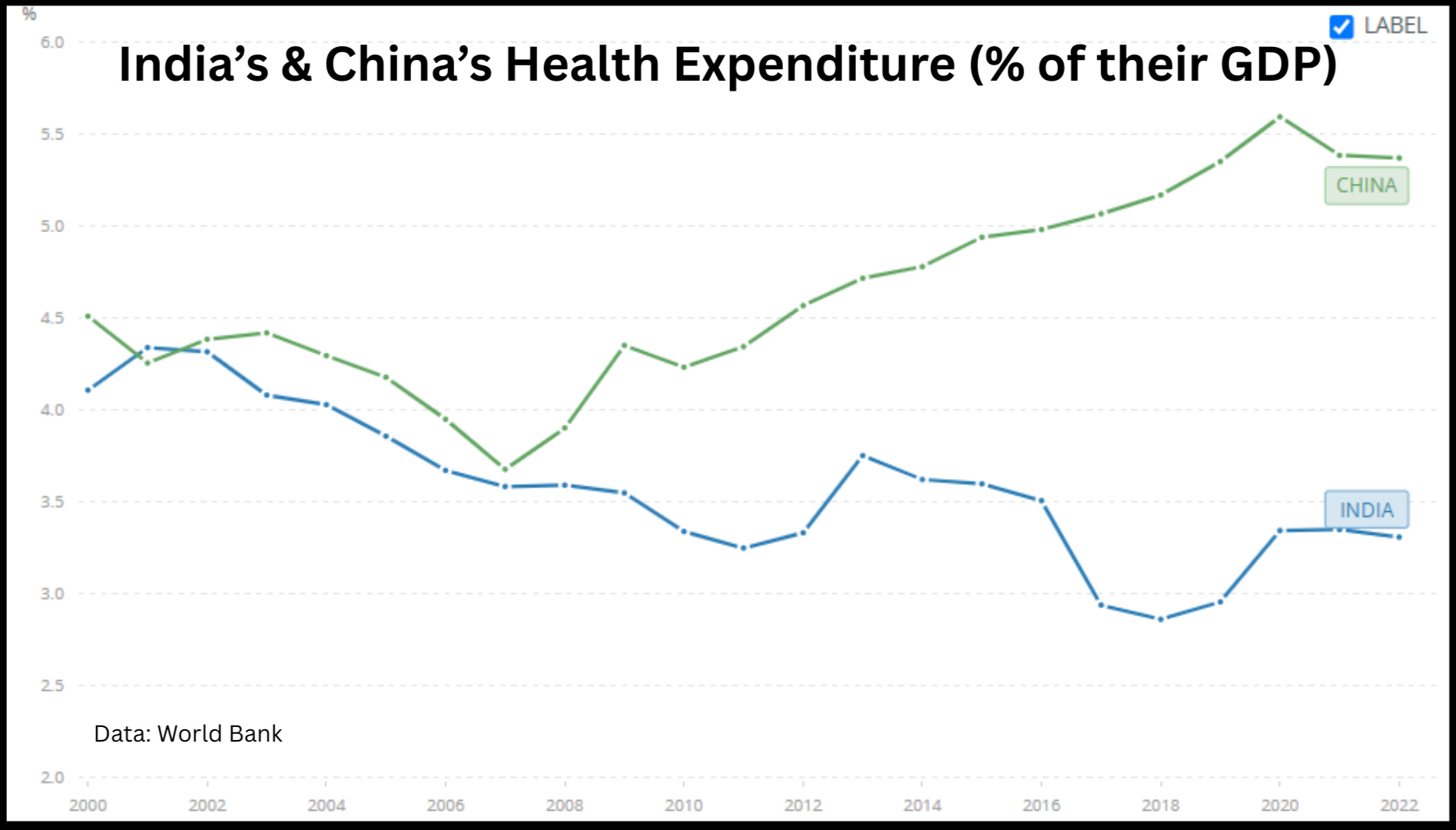

While government’s ambitious schemes like Ayushman Bharat aim to cover the bottom 40% of the population, but the middle 30–40% - roughly 400 million people - are left to fend for themselves. They earn just enough to be ineligible for subsidies but not nearly enough to afford private healthcare without stress. All these elements contribute to the fact that the total health spend as a % of GDP has been falling in last 2 decades and is just 3% of GDP incase of India which is one of the lowest among major economies - making our healthcare system chronically under-resourced.

While in many countries government does the heavy lifting of ensuring that healthcare is adequately funded but this hasn’t been a focus area for Indian government. Developing countries with relatively young population like Brazil & South Africa have this ratio at 9% of their GDP, with China about to reach 6%. Countries like Japan with an old population stand at ~12%. (Source)

How poor affordability impacts quality of healthcare?

Recently, I got to attend a 2-day conference in Mumbai where one of the panel discussions was on ‘India's Medical Devices Journey’. This market for advanced devices is still very small in India, and a small market forces us to import most of our requirements, as no manufacturer is willing to produce such sophisticated devices at a small scale just to cater to domestic demand. India imports most of its high-end and advanced diagnostic machines (like digital X-ray, CT scan, MRI) from companies like Siemens, GE Healthcare, Philips, etc.

During the Q&A session, I got a chance to discuss why this market remains so small despite India being the most populous country in the world - and we concluded that one of the key reasons for the poor demand for technologically advanced equipment is the low penetration of insurance in India. People simply can't opt for better treatment due to their limited ability to pay or restricted insurance coverage.

India has one of the lowest penetration of ‘health insurance’ in world. Our penetration level of just 0.4% of our GDP against 5.6% for USA in 2023.

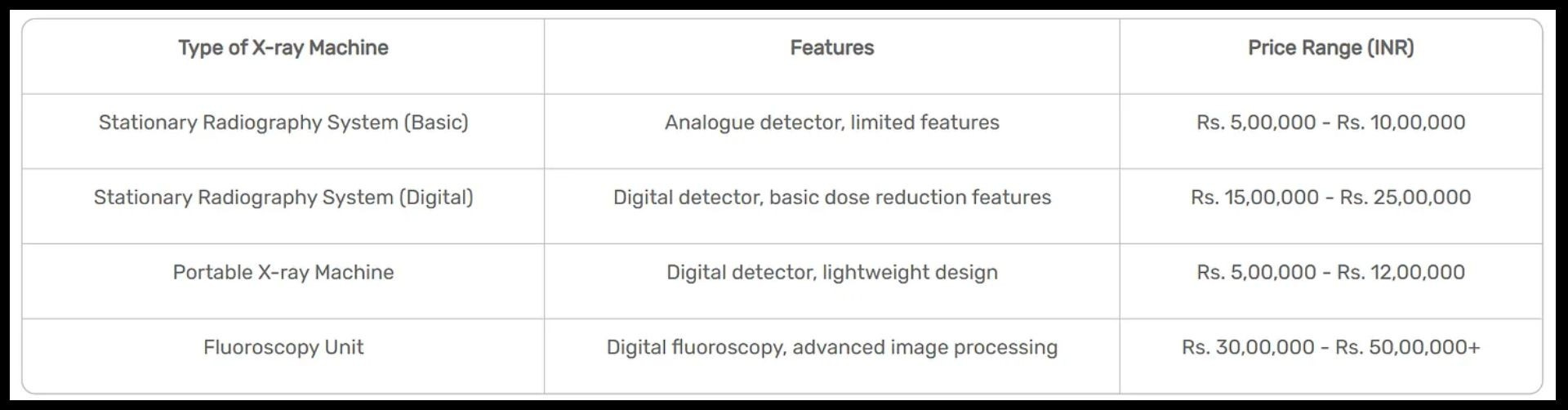

Let’s take the example of a ‘Basic’ X-ray, which might cost you ₹500 per test. On the other hand, using an advanced, accurate, and instant digital X-ray machine might cost you ₹1,500 - ₹2,000 per test. But since your affordability is low and you don’t have insurance coverage, you might end up opting for the former option, especially since you’ll need to do the test a couple of times during your treatment. This is where you indirectly promote the adoption of basic or obsolete machinery, and as a result, the market for high-end and advanced diagnostic machines continues to remain small. Here’s a price list of the best-selling X-ray machines in India, showing how drastically the prices and features vary:

When affordability is low, people often delay or avoid seeking medical help until absolutely necessary, leading to worse health outcomes. Instead of preventive care or early diagnosis, treatments happen at advanced stages, when complications are harder - and more expensive - to manage. Many middle-class families also opt for cheaper, lower-quality hospitals, unqualified practitioners, or cut corners on medicines and follow-up care, all of which directly compromise the quality of healthcare they receive. This creates a vicious cycle where poor affordability leads to poorer care, which then leads to even higher costs and deteriorating health.

Can better insurance penetration help?

Immediately after the panel discussion ended, I struck up a conversation with a fellow attendee who shared her frustrating experience with insurance claims when her dad was recently hospitalized for a week. Despite her dad having insurance, she not only had to pay the full amount upfront in cash to the hospital, but also had to wait several months to receive the claim amount, which was only partially approved. To make matters worse, the insurance broker from whom her dad had purchased the policy was based in Goa at the time and provided very little assistance.

“An insurance company and a hospital have exactly opposite interests which causes the system to have a lack of trust. ”

- Yashish Dahiya, Co-Founder, PB Fintech

In India, around 4 crore people pay insurance premiums with the hope that they won’t face difficulties when they fall ill and visit hospitals. But the reality is far from smooth – customers often face significant challenges – sometimes even more than expected, as the fellow attendee mentioned earlier. High delays in claim settlement, an extensive pre- and post-hospitalization process, lack of communication and transparency, hidden costs, and poor grievance redressal all contribute to bad customer experiences. Hospitals benefit from inflating bills – while such claims result in losses for insurance companies.

When Families Shrink, Vulnerability Grows

Back in 2008, only 37% of Indian households were nuclear, which has now risen to 50% in 2022, implying ~160 million households out of ~320 million households are now nuclear. Infact, as per Kantar’s Consumer Connections 2023 research, 3 out of 4 incremental households in India over the past 14 years are nuclear. Where our average family size used to be above 5 members as per 2001 Census, this has fallen to ~4.4 members in 2021.

Once, extended families stood like a fortress against life’s uncertainties. There was always a senior member in a large family who would step forward to support, or everyone would contribute towards the cause – just like an insurance policy. Today, as families shrink to just two or three earning members, that shield is gone. In a nuclear household, a single illness, a hospital bill, or a sudden job loss can shatter years of careful savings and stability. There are fewer shoulders to lean on, fewer hands to share the burden, and when crisis strikes, it hits harder and deeper. Vulnerability isn’t just a possibility – it’s the new reality for millions of middle-class families.

India is destined for the ‘Private’ path

It took 80+ years for France & Sweden in doubling of its older population with over 60 years age from 7% to 14%, whereas it’s expected to happen in just 28 years in India. By 2061, every fourth Indian might be 60 or older. We are ageing must faster than the trajectory followed by the rest of the developed world. And unlike the West, India will be aging at a time when its per capita income will still be relatively low, making it harder for the healthcare system to support an older population.

While healthcare continues to be a low priority for the government, as reflected by the small percentage of GDP spent on it, even by the time India ages, government finances won’t be sufficient to support the elevated needs of its population.

Impact? India’s healthcare system will, in all likelihood, eventually become a privately-run, profit-driven system similar to that of the United States.

Always For Profit - U.S. Healthcare

In the U.S., healthcare isn’t just about treating people - it’s big business. Unlike Europe which has state-funded universal healthcare, U.S. has a largely privatized healthcare system. Insurance companies make billions every year by collecting premiums and finding ways to pay out less in claims. Hospitals, especially the big private ones, charge eye-watering amounts for even basic procedures, and the prices are rarely clear upfront. Then there are the pharmaceutical companies, pricing life-saving drugs so high that even insured patients sometimes struggle to afford them. From diagnostics to surgeries, almost every part of the system is designed to maximize profits. At the end of the day, it’s not just about healthcare anymore - it’s about who can afford it.

Think of what that leads to?

The country ranks as the worst performer among 10 developed nations in critical areas of health care, including preventing deaths, access (mainly because of high cost) and guaranteeing quality treatment for everyone, regardless of gender, income or geographic location, as per the report by the Commonwealth Fund.

Second Order effect?

In the European market, where governments run hospitals and often negotiate drug/device prices centrally, you’ll not often find big listed insurance or hospital chains. The listed healthcare space is primarily led by pharmaceutical giants such as Novo Nordisk, Roche, AstraZeneca, and companies like Siemens Healthineers and Essilor Luxottica in medical technology and devices – with a key focus on exports.

On the other hand, the USA has a privately owned, for-profit healthcare system, with multiple private players involved in each part of the value chain. Non-pharma companies like UnitedHealth Group, Elevance Health, Cigna Corporation, and HCA Healthcare are some of the biggest listed companies in the country. In fact, it was initially the hefty profits from their insurance business that helped Berkshire Hathaway build its "investment fund" over the years.

Read more about US healthcare here: A Deep Dive on US Healthcare

What PB Health aims to solve in India?

Till now, in this blog, we’ve discussed several instances that highlight how broken the Indian healthcare system is, which are:

Low insurance penetration & financial implications: One hospital bill can wipe out all you career savings if you don’t have adequate insurance.

Limited use of technology: India’s small market for advanced medical equipment disincentivizes innovation for better healthcare in the country, making us heavily import-dependent for most of our needs.

Poor customer experience: Lack of trust between stakeholders (hospitals, insurance, and customers) creates friction, promotes scrutiny, and deteriorates customer satisfaction.

With family sizes shrinking and minimal focus on healthcare by the government, India is destined to follow the U.S. path — a for-profit system that ranks poorly on global parameters due to the existing gaps.

Now, the reason we were excited to write this blog is due to a first-of-its-kind experiment happening in our country. India’s largest insurance aggregator, PolicyBazaar’s parent company, recently incorporated PB Healthcare Services on January 1, 2025, and raised ₹2,000 crore from its parent and external investors to carry out healthcare and allied services in India.

Taking the Road Less Traveled

“I can keep standing outside a large hospital for the next 10 years and never get access to build their tech and experience, I might as well do it rather than waiting outside the gate of the hospital.”

- Yashish Dahiya, Co-Founder, PB Fintech

An internet platform company entering the hospital/healthcare business is reason enough to send alarm bells ringing for its investor community. But those alarms don’t deter the ambitious Yashish, who knows exactly what he wants. While they start by owning a few hospitals to get the model in place, the goal isn’t to own hospitals but to have better control over all the touchpoints that a customer encounters once they’ve taken private health insurance.

India’s first HMO - (Health Maintenance Organization)

This concept originated in the United States in the 1920s and later gained federal support with the signing of the HMO Act by President Richard Nixon in 1973, which encouraged the creation and expansion of HMOs by private players. It became popular in the 1990s as a way to control rising healthcare costs, and today, organizations like Kaiser Permanente operate on this model.

Think of an HMO as being part of a carefully managed club for your healthcare. You have a team of doctors and hospitals you can visit, but you need to stick to the club’s list - the "network." You also choose one main doctor, called a primary care physician, who becomes your go-to person for everything - regular checkups, advice, and even when you need to see a specialist. However, you can’t just walk into a specialist's office; your primary doctor needs to give you a referral first.

“A narrow network of hospitals would help create a full-stack model where the customer experience can be better controlled through vertical integration.”

- Yashish Dahiya, Co-Founder, PB Fintech

With this aim in mind, they plan to start their operations and open their first hospital by December 2025 in Delhi NCR. The first 4 to 8 hospitals will be self-owned, with future hospitals controlled through partnerships. While they will offer customers much less freedom of choice, here are three things they aim to solve:

Bring down the cost of insurance premiums paid by the customer and increase the penetration of health insurance in the country

Better and wider utilization of advanced technology at their controlled hospitals for treatment, leading to better and faster cures

Bridge the trust between insurance providers and hospitals, enhancing the customer experience

To accelerate implementation, they are onboarding global partners as co-owners of this project [Update - General Catalyst investment in PB health as biggest investor] who are equally bullish on Indian healthcare, though the quantum of benefit their flagship platform company, Policybazaar, will gain is still unknown.

To END: More than 2 years ago, we wrote how Policybazaar revolutionized how Indians buy insurance. Today we wrote on how they are aiming to revolutionize how healthcare is delivered in India. Excitement is much higher this time & we shall continue to track it closely in our future blogs.

Connect with us on LinkedIn here: Aditya Grover and Yash Agarwal

Finding Outperformers is a free-to-access website, and each blog takes a month of effort to finalize. If you've read this far and you find our research useful, consider supporting our efforts by contributing here:

Read 2 year year old post when we became bullish on the stock⬇️

Disclaimers-

We are not a SEBI registered advisors; personal investment/interest in shares can exists for any company mentioned above; this isn’t investment advice but our personal thought process; DYOR (do your own research) is recommended; Investing & trading are subject to market risk; the decision maker is responsible for any outcome.

| A guest post by

|