The DLF Story: A Controversial King

Covering all the major controversies surrounding the Real Estate giant since 2005

Recently we went overweight on DLF in our portfolio when mentioning that in our blog talking about the rationale for going overweight on the DLF shares in my portfolio. In the risks section, I touched upon the Robert Vadra - DLF controversy that occurred years ago, in which DLF was accused of acquiring land from Mr. Robert at a very high price, along with many other allegations. This became a big political issue since Mr. Robert is the son-in-law of Sonia Gandhi and was raised multiple times during the 2014 National elections and Haryana elections by the then-opposition parties.

It wasn't just one isolated controversial incident involving DLF; rather, the period from its IPO in 2006 was marked by numerous controversies for India's largest real estate giant. Here are some key cases I plan to discuss:

DLF IPO Controversy around Non-disclosures in DRHP (2006)

DLF - Vadra Land Grab Case (2008)

CCI penalty of Rs 630 Cr for abusing ‘Dominant Position’ (2011)

QIP Non-disclosure controversy (2019)

In addition to these cases, there are several ongoing court cases of lesser significance. Some of these were initiated years ago and remain pending in the Supreme Court or High Court. As we delve into each of the four points mentioned above, I will provide my analysis along with my personal take on each of them, trying to present it with minimal bias, considering I am also a shareholder. It's important to note that real estate is the world's largest asset class, both globally and in India, and is susceptible to occasional new controversies.

Note: If my emails end up in the ‘promotions’ tab, please move them to inbox so you don’t miss out. Don’t forget to subscribe and join 1K+ readers!

DLF IPO Controversy (2006-2007)

DLF had many rivals even before it came out with its IPO in 2007. As per this ET article (DLF IPO - The Untold Story), even a Cabinet minister once had to intervene in this rivalry, warning the rival camp that the camp wouldn’t get ‘certain permissions’ they were seeking if they didn’t back off from stopping DLF from coming up with its IPO. This transpired during the tenure of the UPA government led by the Congress party.

DLF came out with DRHP for its IPO twice (DRHP is a document containing all details of the IPO that the company files with stock exchanges), once in May 2006 and then in Jan 2007. The differences between the two DRHPs became the root cause of our first controversy. The IPO issue was opened for subscription from 11 June 2007 to 14 June 2007, where the company planned to raise about Rs 9,187 Cr.

Exactly a week before, on June 4, 2007, a significant development occurred with the emergence of 'Mr. Kimsuk Krishna Sinha', a man whose actions would forever tarnish DLF's reputation. Mr. Sinha pointed out the differences between the two DRHPs filed by DLF. He indirectly drew attention to the fact that in November 2006, DLF had divested its 355 subsidiaries into three separate entities: Felicite, Shalika, and Sudipti. Intriguingly, all three shareholders of these entities were the wives of key DLF employees (KMPs), with negligible business expertise as per the ex-SEBI chairman. Mr. Sinha alleged that one of these subsidiaries, 'Sudipti', had defrauded him of Rs 34 crores in a land purchase transaction and had registered an FIR against 'Sudipti' in April 2007. He further asserted that 'Sudipti' should be considered a deemed subsidiary of DLF because the company still had indirect control over it through its employees' wives. Consequently, he requested SEBI to disallow the listing of DLF shares and take immediate action due to non-disclosures by the company, all in the interest of protecting the general public.

This controversy persisted for several years, and in 2014, after numerous legal proceedings, SEBI concluded that DLF and its promoters were at fault. It imposed a three-year ban on 6 key individuals, including the Promoters, the MD, the CFO, and the Executive director, from accessing financial markets. Following this, DLF appealed to the Securities Appellate Tribunal (SAT) against SEBI's ban, and SAT upheld the company's appeal, overturning SEBI's order within a few months. Ultimately, SEBI imposed a penalty of Rs 86 crores on DLF and related entities

(If you wish to understand this controversy in detail, the 2 sources I recommend would be this report by Stakeholders Empowerment Services on DLF Limited and this detailed discussion between 2 legal experts and ex-SEBI chief on YouTube ^)

My take: Now comes the toughest part for me to comment on this. Many experts have highlighted the notion of materiality in this case, and I tend to agree with this perspective. A new legal case seeking Rs 34 crore in compensation for a company that is raising over Rs 9,000 crores and had a land bank valued at Rs 90,000 crore in 2005-06 by Cushman and Wakefield appears relatively insignificant. As an investor, this amount wouldn't be a significant concern.

It's widely acknowledged that real estate companies often create multiple subsidiaries with different names to facilitate negotiations when acquiring assets, such as land or buildings. This approach does add complexity to the corporate structure. If DLF Ltd, as the parent company, were to directly purchase land from small landowners, it's clear that those sellers would demand higher prices due to the brand name involved. The decision to transfer those 355 subsidiaries away from their books might have been an attempt to simplify the company structure in preparation for the IPO. The biggest issue that impacted here was that this ‘case study’, irrespective of the small amount involved, became a headline case study in various discussions that happened between many professionals later, hence badly damaging the reputation of the promoters of DLF for years to come.

DLF - Robert Vadra Land Grab Case (2008)

This case has multiple angles to it involving several kinds of allegations including significant claims from 2012 made by the then-opposition BJP and emerging political figures like Arvind Kejriwal, who later became the Chief Minister of Delhi. The central allegation, supported by quantifiable figures, revolves around the purported illegal profit of Rs 50 crore that Robert Vadra amassed in a matter of months when DLF acquired a land parcel from him for approximately Rs 58 crore in 2008. Interestingly, Robert Vadra received around Rs 8 crore from DLF as advances to secure that land from the government, in the first place.

DLF defended itself by asserting that it was a common practice for real estate companies to provide advances to select individuals who would assume the risk, acquire land on DLF's behalf, and subsequently sell it back to DLF at appropriate rates, compensating them for the "risk" they undertook. I am dropping a link to a recent interview of Mr. KP Singh, the promoter and largest shareholder of DLF justifying how the land grab wasn’t a scam, rather it was how the business used to happen before. He also mentions that it wasn't just Mr. Vadra from whom DLF purchased land; his name gained prominence due to his association with the Gandhi family. In reality, many other individuals, whom he referred to as "smart guys," acquired land in strategic locations that DLF had to later purchase at higher prices, ultimately enriching themselves in the process. These other individuals' names didn't surface in the same way since they lacked the high political profile that Mr. Vadra enjoyed.

Additional allegations made by political parties included Robert Vadra's investments in DLF projects and properties in the Delhi NCR region. There was also a focus on Robert Vadra's purchase of apartments constructed by DLF, which was seen as a gesture of gratitude towards the Haryana government for the favors they allegedly received. In response, DLF consistently maintained that their dealings with Mr. Vadra were in line with standard business practices, and they denied having received any illegal benefits or favors from the Congress government.

Over the years, a series of events unfolded, including a CAG (Comptroller and Auditor General) Report, the establishment of the SN Dhingra Commission by the BJP government to investigate, CBI chargesheets, the involvement of the Enforcement Directorate (ED), and numerous cases in the High Court and Supreme Court. These events continued to impact DLF's reputation adversely year after year.

The Congress party had a counter-allegation, arguing that, until 2014, various state governments, including the Congress-led Hooda government, had approved a total of 11,000 acres of land in Gurugram. They contended that the BJP government's focus on investigating cases related to just 63 acres of land, with only around 3 acres allocated to Mr. Vadra, was a selective approach. This selective focus led the BJP to establish the Dhingra Commission to investigate these specific land dealings. Dropping the YT link below: [Update - The video has been turned private by the source now after this blog was published, not sure why this happened]

In a recent relief to DLF, the BJP-led Haryana government informed the Punjab and Haryana High Court in Chandigarh in April 2023 that they did not find any violation of rules or regulations in the transfer of land from businessman Robert Vadra's Skylight Hospitality to the real estate giant DLF. This development certainly benefits DLF, but it's worth noting that the case is still ongoing, and further proceedings are expected.

Note: Haven’t subscribed yet? it’s a click away, go ahead and subscribe now!

My take: I do feel that here again, the concept of materiality must be kept in mind as an investor of DLF. The amount of Rs 50 Cr that Mr. Vadra gained from this case is irrelevant, the real concern is the negative image that DLF has been dealing with since it became a political issue in 2012. Various political parties continue to blame DLF, which has tarnished its reputation. The practice of land allocation to developers through bidding and lottery systems by district development authorities has significantly improved across India over years. This reduces the scope of future scams and corrupt practices.

As court cases related to this issue remain unresolved for years, it's difficult to predict if DLF will face any repercussions that could harm its business. I believe that this is more of a politically driven case, and DLF simply had the misfortune of purchasing a 58 crore rupees piece of land from Mr. Vadra. This amount is a mere 0.065% of the total land bank valued at around 90,000 crore rupees that the company was owning back then.

CCI penalty of Rs 630 Cr for abusing ‘Dominant Position’ (2011)

The dispute in question originated in 2010 when flat buyers' associations from three DLF development projects in Gurgaon—DLF Magnolias, Park Place, and the Belaire—lodged complaints with the competition regulator. They alleged project delays and the construction of more floors than originally planned, among other issues.

In 2011, the Competition Commission of India (CCI) issued orders imposing a penalty of Rs 630 crores on DLF Limited. The penalty was related to DLF's alleged use of unfair conditions with buyers in Gurugram and unauthorized construction of additional floors without notifying the buyers. DLF contested the CCI's orders in the Competition Appellate Tribunal (COMPAT) and then in the Supreme Court. The top court instructed DLF to deposit the fine amount with them until a final verdict was reached. As of the present date, the case remains pending. (Source: Annual report 2022-23, Page 145/448)

Back in those times, the practice of altering project details after sales were not uncommon. In 2012, CCI was reportedly investigating over 70 real estate companies in India for alleged collusion as per the ET article but no major orders were passed in the years that followed. DLF, being the biggest of all, even alleged that it is “very surprising” that no penalty has been imposed on other realtors operating in the same market with the same product line. One may note, that CCI did impose a fine on Jaiprakash Associates in 2019 for abusing its dominant market position by imposing ‘unfair’ and ‘discriminatory’ conditions on home buyers but the amount fine was a mere Rs 14 Crore. Even in 2015, two members of CCI proposed to impose a fine of Rs 666 crore on JP Associates in a similar case, but that never happened as the Chairman and other members of the regulatory body overruled the proposal with a 3-2 majority in the panel of 5 members.

My take: In light of the implementation of RERA - Real Estate (Regulation and Development) Act, 2016, developers now have limited options for altering project details. Any changes require the permission of home buyers in many cases. All projects must be listed with complete details on RERA before being offered for sale. This law has been instrumental in ensuring the timely completion of projects, safeguarding the interests of buyers, and reducing the likelihood of facing legal cases and penalties in the future.

It's worth noting that, unlike Jaiprakash Associates, which faced bankruptcy and failed to deliver projects to its buyers, DLF successfully completed all three projects: DLF Magnolias, Park Place, and the Belaire. If you were one of the complainants back in 2010 and still own your flat, congratulations! You are now among the wealthiest individuals in the Delhi NCR region. The value of these properties has appreciated significantly over the years. For instance, in the case of 'The Magnolias,' flat prices now start at around Rs 25 - 30 crores, representing a doubling in value just over the past two years. According to an analysis by Ankur Warikoo’s team on luxury properties in Gurugram, all three projects rank among the top 10 most luxurious projects in Gurugram, with 'The Camellias' leading the list.

QIP Non-disclosure controversy (2019)

This is the last major allegation that I will be discussing, which was relatively short-lived.

In March 2019, DLF completed its QIP of over Rs 3,000 Crores in which major institutional investors who have participated including UBS, HSBC, Marshall & Wace, Myriad, Key Square, Goldman Sachs, Indus, Eastbridge, Tata Mutual Fund and HDFC Mutual Fund and was subscribed over two times.

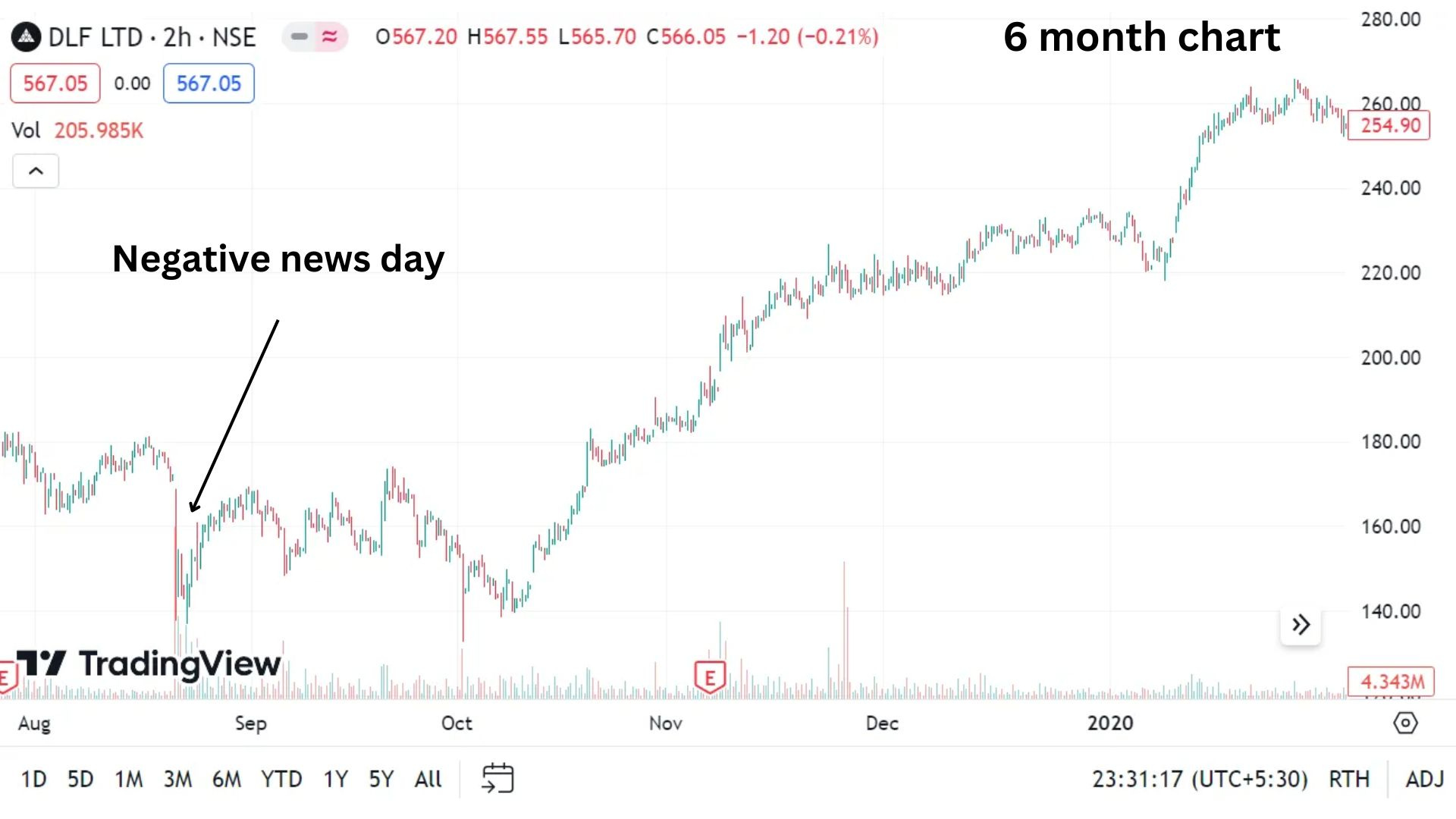

In August 2019, an allegation emerged that DLF had failed to disclose an amalgamation, making one of DLF's flagship subsidiaries potentially liable for matters related to court orders concerning M/s Aaliyah Real Estates. This allegation also accused DLF of suppressing vital information. The Supreme Court issued a regular notice to DLF, requesting clarification on this matter. As a result, DLF's stock price dropped by over 20% during the trading day and closed approximately 16% lower by the end of the session. The company denied all allegations.

Interestingly, the petitioner who raised this issue at the Supreme Court was the same individual who had raised concerns during DLF's IPO in 2007 about the non-disclosure of a subsidiary by DLF in its Draft Red Herring Prospectus (DRHP), who is: Mr KK Sinha or ‘Mr. Kimsuk Krishna Sinha’ as per news reports. Here is the response from Mr. Ashok Tyagi, the then CFO and now CEO and Whole-time Director of DLF:

My take: I won’t comment much on this issue as it was short-lived and market share price action in later months itself is a response that approximately doubled in the next ~ 6 months time period:

Final Take

Running a property business can be challenging, particularly without strong political connections. DLF, in particular, had to establish solid ties with the Congress government for many years before 2014, both at the state level (Haryana) and central level. However, things changed when the opposition took power in the next decade (BJP and AAP) and now they had to deal with new people. It's difficult for an outsider like me to gauge the extent of these political connections. Nevertheless, it's worth noting that since 2014, when the BJP came to power at both levels, DLF hasn't faced any major new legal cases, and it hasn't been found guilty in the last decade. Though the court cases linger on.

Promoter KP Singh now lives in London and is not involved in the business activities. His son, Rajiv Singh, who currently manages the business, rarely appears in the media. During this time, Mr. Ashok Kumar Tyagi, who joined DLF in 2008 and is now the CEO and Whole-time Director, has been the public face of DLF for the investor community. The team's efforts to improve disclosures year after year are commendable. Notable improvements include disclosing tenant mix and rental rates per square foot at various retail rental properties, especially following the investment by Singapore's GIC in 2017. Another minor but positive change is the availability of analyst conference call recordings and transcripts on their website, which wasn't the case before the COVID pandemic. This surely makes life easier for a researcher like me :)

All in all, I do feel DLF did get a bit unlucky. It was the only player who got punished by CCI out of 70 others (as reported by ET). Its IPO controversy started in 2007 and continued to tarnish its reputation till 2015 when SAT overturned SEBI’s order. A small deal with Mr. Robert Vadra caught national headlines on a daily basis as political parties continued to attack them for years and whatnot.

On a Separate Note

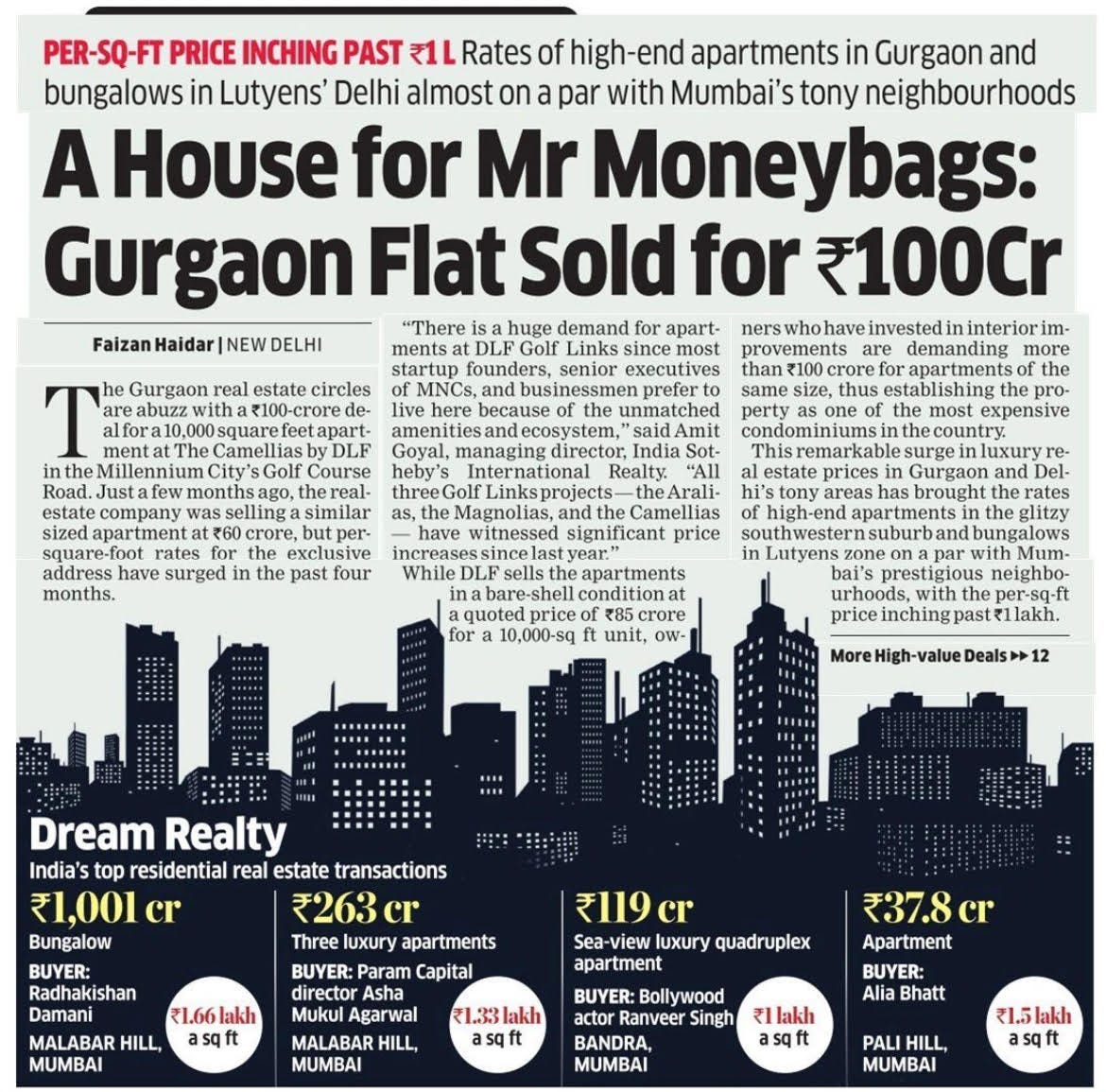

Recently, at DLF’s most luxurious project in Gurugram: The Camellias, a flat was sold for Rs 100 Cr which matches the rates of posh areas of Mumbai and New Delhi. The rates along Golf Course Road have been skyrocketing in the last 2 years as I pointed out in my previous post. This is great news for them as they plan 2 more luxury projects within the next 5 months, both in Gurugram.

Thankyou for reading till here. It takes significant efforts and time of mine in producing this blog on my own. Consider sharing with your friends and help me reach more audiance which acts as a motivation for me.

If you haven’t checked out my previous blog on DLF written a month ago when I went overweight on DLF in my portfolio, consider giving it a read! -

Luxury & Class: Brand DLF

"Some years ago, Camellias flats used to begin at around Rs 30 Crores, and I remember thinking how exorbitant those prices were. However, today, the same Camellias flat starts at Rs 45 to 50 Crores, illustrating the substantial increase in prices post-COVID-19 pandemic," shared

Enjoyed reading such a detailed article and getting to understand your unbiased take on these controversies and I liked how you have supplemented your article with sources and videos which add weight to your article.

Excellent. Keep making such nuanced analyses.

Will surely bet on your PMS once you have it :P