Will Nazara receive a GST notice?

Emerging risks and recent happenings of India's only listed Gaming company

Hi Reader, as the year 2023 comes to an end, we look back at the setbacks faced by many gaming companies in India in 2023.

In September 2022, Gameskraft Technology, the owner of popular games like RummyCulture, Pocket52, and Ludo Select, received a show-cause notice from the GST department. The notice alleged a failure to pay Rs 21,000 crore in GST, marking the largest claim in the history of indirect taxation. The specified period for the notice was between June 30, 2017, and June 30, 2022, as GST was implemented from 1st July of 2017. Subsequently, Gameskraft contested the notice in the Karnataka High Court, and in May 2023, the court dismissed the department's notice.

The court ruling clarified that the GST department couldn't apply tax to the company by classifying Rummy as a 'game of chance'; instead, it recognized it as a 'game of skill.' This legal distinction is crucial because games of skill attract an 18% GST on gross gaming revenue, while games of chance incur a 28% GST on the total bet value. The difference not only lies in the tax rate but also in the base to which the rate is applied.

For instance, if a gaming platform is classified as a game of 'chance,' and a player deposits Rs 100 to bet, the platform must collect Rs 28 from the player and remit it to the GST department. Consequently, the player can only bet with the remaining Rs 72. Conversely, if the platform is categorized as a game of 'skill,' there is no tax on the initial Rs 100 deposit. Instead, an 18% tax is levied on the revenue generated by the platform from betting. For instance, if the platform makes Rs 5 in revenue, the GST of 18% is applied only to that amount, resulting in approximately Rs 1 in tax—a significant reduction compared to the 'chance' category scenario.

In practical terms, platforms categorized as 'chance' might need to deposit 28 times more GST amount to the government compared to those categorized as 'skill.'

Note: If my emails end up in the ‘promotions’ tab, please move them to inbox so you don’t miss out. Don’t forget to subscribe and join 500+ readers!

The regulatory landscape evolved further as of October 1, 2023, with the government implementing a new rule. Regardless of whether a game is categorized as 'chance' or 'skill,' a uniform 28% GST will be applied to the total betting value of Rs 100, requiring a submission of Rs 28 to the government. It's important to note that the discussion around the GST notice mentioned earlier, and those to be discussed subsequently, pertains to the period before October 1, 2023. During this time, real money gaming (RMG) companies like Gameskraft, with support from various high courts, asserted their classification as 'Skill' entities. However, the government persisted in arguing that they fell under the 'Chance' category.

In a noteworthy development, the Kerala High Court had overturned the state government's ban on games of chance, such as online Rummy, in 2021. The court's ruling stated that online Rummy qualifies as a game of mere skill.

Presently, the GST department remains unconvinced by these arguments and has escalated the matter to the Supreme Court, challenging the favorable judgments from state courts in support of Gameskraft and other RMG companies. The department continues to issue show cause notices to RMG (real money gaming) companies. Below is a list of companies that have recently received such notices, including Gameskraft with its Rs 21,000 crore demand:

Dream11: Rs 28,000 Cr

Play 24/7 (parent of Rummy Circle, My11 Circle): Rs 20,000 Cr

Deltatech Gaming (parent of Adda52.com): Rs 6,300 Cr

Head Works Digital (parent of A23 Rummy): Rs 5,000 Cr

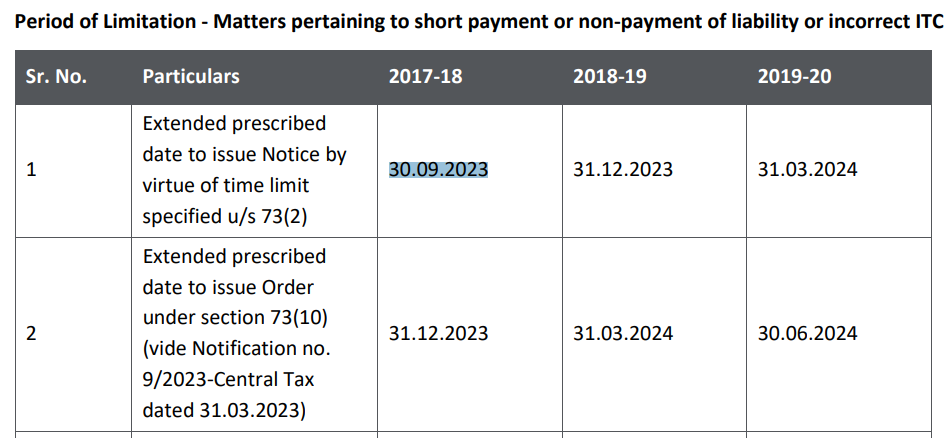

Majority of these notices to the aforementioned companies were dispatched in the second half of September. This timing aligns with the deadline for the department for issuing GST show cause notices for cases related to the FY 2018 under section 73(2) of GST, which was set for September 30, 2023. Following this timeline, the deadline for sending notices for the financial year 2019 is officially December 31, 2023, and for the financial year 2020, it is March 31, 2024, as per the provisions of section 73(2) of GST. In essence, one can anticipate more such notices pertaining to the FY 2019 and 2020 and after, being dispatched by the department in the coming months, but not related to FY2018. Here is a Deloitte report discussing why spurt of notices happened as the deadline for the department approached:

And as per section 73(10) stated in row 2, post 31st December, 2023, any possible tax demand, penalty, etc pertaining to FY18 will be considered as waived off. Similar dates for FY19 and FY20 are given above.

Will Nazara get a notice too?

As we have set the background for you above, we now come to our portfolio company Nazara Tech which too has 2 major subsidiaries in real money gaming (RMG) space namely HalaPlay and Openplay (parent of Classic Rummy). They owned HalaPlay before listing, and acquired Openplay in 2021. Here is how the revenues for both the entities from FY19 to FY23:

The trend reveals a consistent decline in share of HalaPlay over the years. In cumulative terms, HalaPlay generated approximately Rs 85 Crores in revenues, while Openplay recorded around Rs 207 Crores from the FY 2019 to FY2023. Despite Openplay's acquisition happening only in the fiscal year 2022, it's essential to consider that the GST department might not differentiate between pre and post-acquisition periods when issuing notices to Nazara, the parent company. Typically, liabilities like GST demands are transferred to the new owner at the time of acquisition unless explicitly stated otherwise. Consequently, Nazara could be solely responsible for addressing any GST demands throughout Openplay's entire operational history.

In the last five years within the real-money gaming (RMG) sector, Nazara Tech appears to have generated approximately Rs 300 Crores in revenues. This raises the possibility of Nazara receiving a GST show cause notice in the future. It's important to note that this estimation is based on revenue data from peer RMG companies obtained from the Ministry of Corporate Affairs (MCA)/PrivateCircle.

Note: Ideally, such estimates would be more accurate if based on the betting amount. However, due to the absence of declared betting amounts by these companies during this period, revenue data serves as the closest available approximation. (Source: BSE filing, annual reports, investor presentations)

How big amount of notice can we expect?

We shall perform a peer company analysis to estimate the quantum of GST notice based on revenues those competitors made in last 6 years and the GST notice they received. We downloaded the financials data of our competitor set namely: Dream11, Gameskraft, Play 24/7, Head Digital Works and Deltatech Gaming, from MCA and other sources including annual reports and management’s interviews. For Dream11 and Gameskraft since they haven’t filed their FY23 financials with MCA, we had to estimate their revenue growth figures based on previous years growth trajectory.

Dream11 has been a clear leader in this space over the years and continues to be due to its popularity and large audience on its platform, followed by Gameskraft which owns RummyCulture.

Next Steps: Understanding the duration for which the GST notices have been issued to each player is indeed crucial for a precise estimation. It's evident that the assessment periods vary, adding complexity to the analysis. Your method of assuming June 2022 as the ending month for three players in the absence of specific information from news articles is a reasonable approach.

Here's a summary of your period data after assessment:

Gameskraft:

Notice Period: July 2017 to June 2022

Deltatech Gaming:

Notice Period: July 2017 to November 2022

Dream 11, Play 24/7, Head Digital Works:

Assumed Notice Period: July 2017 to June 2022

This standardized assumption for Dream 11, Play 24/7, and Head Digital Works based on a 5-year period aligns with the completion of a full assessment cycle.

However, it's important to note that such assumptions, while necessary for analysis, may have an impact on the accuracy of the GST liability estimation. If possible, one might want to continue monitoring news sources for any updates or clarifications on the assessment periods for the other three players.

Here is our data after assessment:

Following the assessment mentioned earlier, we determined an average multiple of 4 times. This multiple was then applied to Nazara Tech's revenues from the real-money gaming (RMG) segment over the last 5 years until FY23, amounting to Rs 300 Crores. Consequently, our estimation arrives at Rs 1,200 Crores

Assumptions and Limitations

Range of Revenue Multiple: The range of revenue multiple derived in our analysis spans from 1.5 times to a high of 8.8 times. This translates to a potential notice amount ranging from as low as Rs 450 Crores to as high as Rs 2,640 Crores, which notably is half of Nazara Tech's current market capitalization.

Assumption of Similar Business Models: A fundamental assumption is that peers share a similar business model. However, it's acknowledged that comparing a sports fantasy business with a rummy/poker betting business might be a substantial assumption. Despite differences, the commonality lies in RMG companies earning revenue as a percentage of the betting pool brought in by players.

Varied Revenue Models for Large and Small Players: The revenue-earning approach for large players may differ from that of smaller players due to their wider reach and larger user base. Deltatech, being the smallest in our peer universe by revenue, exhibits a significant GST amount for its RMG business, resulting in the highest revenue multiple. Size considerations, therefore, can impact results, potentially negatively for Nazara.

Confusion Over GST Notice Periods: Official GST notices are not publicly available, leading to estimations regarding the duration for which notices have been issued. This impacts our ability to accurately calculate revenue during the related tenure.

Inclusion of Non-RMG Players: Some peer players have revenue streams beyond RMG, but without a breakdown available, we had to assume that the majority or maximum data is derived from their RMG business. This can push their multiples lower due to higher base (revenues)

Unavailability of Betting Amount Data: The unavailability of betting amount data for peers' platforms or Nazara's RMG subsidiary complicates the analysis. The exception is Gameskraft, where the betting amount is known due to ongoing discussions and case outcomes over the past year.

In an ideal scenario, access to the 'betting' amounts on peers' platforms or Nazara's RMG subsidiary would significantly simplify and enhance the accuracy of our analysis. Unfortunately, such detailed data was only available for Gameskraft over a specific period due to extensive case discussions in the past year, and not for the peers.

Where do we stand now? What next?

As of the current status, the Gameskraft case is pending in the Supreme Court, where the court will determine the legitimacy of the GST department's tax demand. Given the two separate verdicts from different High Courts favoring gaming companies, the likelihood that the Supreme Court would not uphold them is low. The outcome of this case is anticipated to set a precedent for ongoing and future cases across the country. If the court favors the real-money gaming (RMG) companies, the probability of Nazara receiving a notice becomes almost negligible.

Additionally, it's noteworthy that the deadline of September 30, 2023, for the GST department to issue notices for the FY 2018 has already passed. Looking ahead, the deadline for notices related to the FY 2019 is December 31, 2023. Therefore, any fresh notices received by RMG companies in the coming year would likely be related to the fiscal year 2020 or thereafter.

These considerations add a layer of complexity to the estimation process and highlight the importance of monitoring legal developments and deadlines, as they significantly impact the potential outcomes for Nazara Tech and other RMG companies.

On a Separate Note…

As we maintain our investment in Nazara and refrain from selling any shares in our portfolio, we stay vigilant on the company's operational developments. Two noteworthy updates have piqued our interest (apart from Zerodha’s founders investing into Nazara), involving its subsidiaries Sportskeeda and Nodwin Gaming:

CricRocket: Sportskeeda has introduced an initiative named CricRocket for the ongoing Cricket World Cup 2023. This Android-exclusive app stands out for its rapid delivery of score updates. During personal testing, it proved faster than live TV scores by over 1 ball and outpaced popular cricket websites and Google scores by 1 to 2 balls through AI.

On the performance front, the app has garnered a positive response with an average rating of 4.4 stars. It swiftly reached over 100K downloads within a few weeks of its launch, with the current download figures expected to be significantly higher as the tournament progresses. Notably, CricRocket does not involve fantasy or real-money gaming aspects like Cricket.com, indicating a focus on future monetization through advertisements.

BACARDI NH7 Weekenders

The renowned 3-day event in Pune is scheduled for December 1-3, 2023. In 2021, Nodwin, a subsidiary of Nazara, acquired gaming adjacent IPs and gaming talent business from OML Entertainment for INR 73 Crores. Among the key IPs obtained was the BACARDÍ NH7 Weekender, often described as "India's answer to Glastonbury" by The Guardian. These events have become lucrative, particularly post-COVID, owing to increased demand for concerts and events, thanks to they being Instagrammable :)

BSE filing at time of acquisition shows that this business used to make a revenue of ~Rs 90 Cr (Pre-covid) in FY20 which dipped in FY21 due to Covid-19 restrictions. The current revenue run-rate is unknown as Nazara/Nodwin don’t declare results separately for this segment, but our expectation is it can be somewhere in range of Rs 100 to 150 Cr in FY24 as concerts like these continue to attract big crowds. Here is the teaser for upcoming event is out with its lineup:

That’s all for this one, see you in the next one!

Thankyou for reading till here. It takes significant efforts and time in producing this blog. Consider sharing with your friends and help us reach greater audience.

Note/Disclaimer: I am not any investment advisor (SEBI), and this blog isn’t an investment advice, but how I research around my portfolio companies before investing my own money in them. DYOR (do your own research) before investing is recommended

| A guest post by

|