Is Bharat Ready to Buy? (Part 2)

Rise of Women-Focused Cash Transfers in India: Time to Bet

In early 2017, buried deep inside Chapter 9 of the Economic Survey, released just before the union budget, a bold idea quietly emerged: Universal Basic Income (UBI). Given India’s status as a developing economy with constrained fiscal space, the Survey did not advocate a full-scale rollout. Instead, it suggested a more targeted approach - starting with women. The argument was both economic and social. With limited fiscal headroom, the state should aim for the person most likely to use every rupee wisely: the women.

It was estimated a UBI of ₹7,620 per person annually, covering 75 percent of the population, would cost nearly 5% of GDP. By limiting the program to women, the cost would halve to ~2.5%. Expected to spend more on food, health, and education, women have stronger intra-household bargaining power, and to avoid temptation/sin goods.

In this Part 2 of our series ‘Is Bharat Ready to Buy’, we discuss why we are positive on mass consumption growth beyond Tier 1 cities, where women are emerging as key drivers of India's next major consumption boom. We shall also discuss two listed stocks via which we are increasing exposure of our portfolio in this space to benefit from this structural trend. So grab your cup of coffee, as today’s blog is a long one.

Let’s get started!

Incase you haven’t read the Part 1 yet, would recommend doing so by reading it here before you start reading this part.

India’s Growing Welfare Bill

When UBI was proposed in the run-up to the 2017–18 budget, the Economic Survey flagged an important caveat: the fiscal room required for such a program would only be possible if existing welfare schemes were rationalised. The goal was not to dramatically expand the welfare bill, but to replace fragmented in-kind support and subsidy systems with a more direct, transparent, and empowering alternative.

Total spend on Centrally Sponsored and Central Sector schemes, including programmes like PDS and MGNREGA scheme, was about ₹8.2 lakh crore, amounting to whopping 5.2% of its GDP at the time, while UBI remained only a discussion at the central level

Fast forward to today, the spend on Centrally Sponsored and Central Sector schemes has grown to ₹21.5 Lakh Crores, as budgeted for FY2025–26. This amounts to roughly 5.9% of India’s GDP. Among these is PM-KISAN, launched in 2019, under which over 10 crore farmers receive ₹6,000 annually as an unconditional cash transfer, paid in three instalments through the year. This translates to over ₹60,000 crore in direct income support annually, flowing straight into the bank accounts of rural households across the country - a scale that is both economically significant and politically sticky.

Another big reason for increase in spend on centrally sponsored schemes has been the free grain scheme called Pradhan Mantri Garib Kalyan Anna Yojana (PMGKAY) one of the world’s largest social welfare initiatives, ensuring food and nutrition security for over 81 crore people in India. Centre is currently spending about ₹11.80 lakh crore over five years, with an annual food subsidy of around ₹2.13 lakh crore in this scheme.

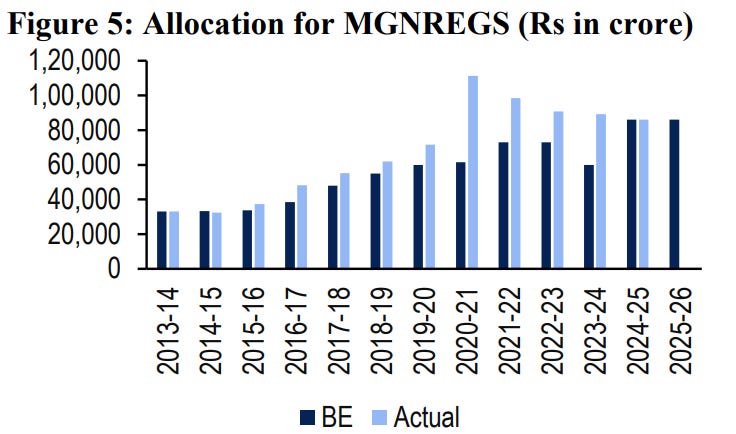

Similarly, expenditure on the Mahatma Gandhi National Rural Employment Guarantee Scheme (MGNREGS), which provides 100 days of guaranteed wage employment in a financial year for adults in rural households, has continued to grow at a healthy 8% CAGR over the last 12 years of the NDA government. This is despite the fact that the scheme was originally launched in 2006 by the current opposition, the Congress-led UPA alliance.

But amidst all this, UBI never formally took shape at the central government level, and the focus remained on expanding spending through Centrally Sponsored and Central Sector Schemes.

What Centre didn’t do, States want to lead on exactly that!

In Part 1 of our blog, we discussed how, despite the poor financial position of several states, many have launched Direct Income Transfer schemes in various formats, with an annualised spend of around ₹2 lakh crore across ~15 states by the end of FY2024–25.

This is about 0.6% of our national GDP being spent, which could increase to 1% of GDP as we close Financial Year 2025-26. Bigger question is how are they funding this incremental expenditure?

Answer - Substituting the capex & other infra spent.

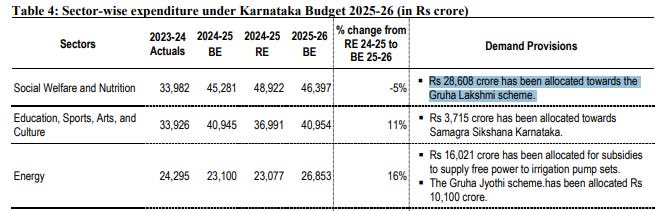

Let’s look at a recent controversy of Karnataka which now spends about Rs 28,608 crores on its flagship Gruha Lakshmi scheme wherein eligible women who are recognized as the head of the family receive ₹2,000 per month. This spend now tops their state budget expenditure list.

Karnataka’s ‘Roads or Rice’ Controversy

Recently on July 5, 2025, a fresh political row erupted in Karnataka after Basavaraj Rayareddi, MLA and economic adviser to Chief Minister Siddaramaiah, made a controversial statement during a public event in Yelburga. He suggested that residents should choose between development (such as building roads) and welfare guarantees like free rice under the ‘Anna Bhagya’ scheme.

“Say you don’t want rice or anything, if you say, ‘only build village roads’, we will do that too. I will suggest to the Chief Minister that our people don’t need rice or anything else, they need this road. Should I tell him?”

- Basavaraj Rayareddi, Economic Adviser to CM, Karnataka

He further explained that with limited government funds, not all demands such as roads, welfare schemes, and temples can be met at once. He implied that if villagers wanted roads to be prioritised, they would need to forgo some welfare benefits and these remarks laid bare the underlying financial pressures faced by the state and triggered sharp criticism from the opposition BJP, which accused the Congress-led government of ‘bankruptcy’ and failing to deliver on both welfare and development fronts.

Hence, CM Siddaramaiah had to come out and reaffirm that the government’s welfare guarantees, including Anna Bhagya, which provides free rice to millions of low-income families will continue and there is no shortage of funds for development.

This situation is not unique to one state but is the case with even wealthy states like Maharashtra which is spending over Rs 40,000 Crores on their flagship women income transfer scheme: Ladki Bahin Yojana.

This tension between welfare and development is no longer theoretical. The original idea behind UBI was to consolidate fragmented subsidies and redirect existing welfare spend into a cleaner, direct transfer system. But what we are witnessing instead is the layering of cash transfers on top of existing welfare, without any rationalisation of previous schemes. The result is not a substitution of one type of welfare for another, it is the substitution of capex for welfare.

Hence, India's development model may well be tilting toward consumption-first economics, where the government transfers becomes the primary driver of rural demand, even if it comes at the cost of long-term infrastructure creation.

2nd Order Effect: Real Wages Set to Rise

As highlighted in our earlier blog ‘India’s Labour Advantage is Slipping’, India could be now entering a period of tight labour availability in urban and informal sectors as lesser people travel from rural to cities for jobs, with the cash transfer playing a big role & could trigger a consumption boom (esp of staples) in years to come.

One of the ways we can track how consumption is doing in the country is via how the Nifty FMCG index has been performing in the markets. This is a sectoral index that tracks the performance of India’s top listed companies like Hindustan Unilever (HUL), ITC, Nestlé India, Britannia, Dabur, Marico, & Godrej Consumer Products.

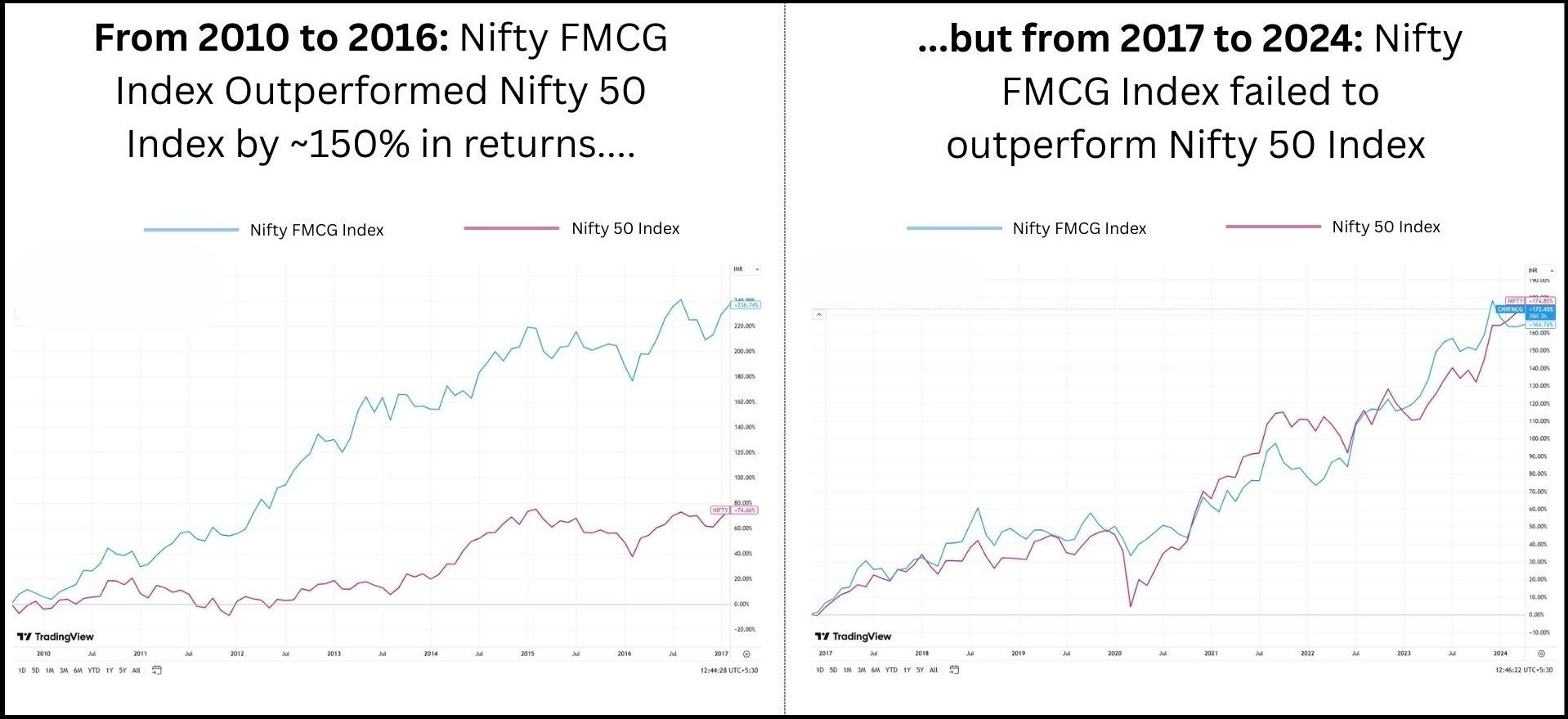

From 2010 to 2016, these stocks were the market's most consistent compounders. The Nifty FMCG index outperformed the Nifty 50 by over 150%, driven by rapid rural premiumisation, real wage growth and a supportive inflation backdrop. However, between 2017 and 2024, this outperformance faded. The sector lagged broader indices as wage growth decelerated, new-age consumer D2C startups stole investor attention, and urban consumption shifted to premium discretionary categories.

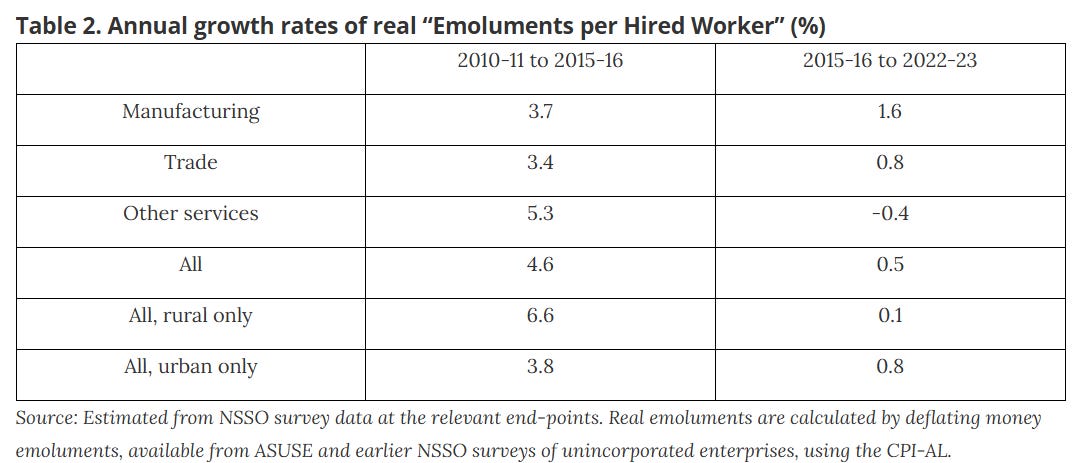

Between 2010 and 2016, real wages in India grew at a healthy pace, with rural wages rising by 6.6% annually and overall wages by 4.6%. In contrast, the period from 2016 to 2022–23 period, we saw a sharp deceleration in growth rate, with rural wage growth collapsing to just 0.1% per year, while overall wage growth dropped to 0.5%. This slowdown directly impacted the spending power of India’s bottom 40%, especially in rural areas where most FMCG demand originates.

Low growth in wages significantly slows down the formalisation of consumption and therefore the packaged goods penetration, which is crucial for FMCG companies to outperform.

“….(On reason for low growth) is a slowdown in wage growth of the non-salaried workforce in urban areas, which has risen 3.4%, slower than inflation.”

- MD Varun Berry, Britannia (Nov 2024) (source)

This is what we expect to change soon. With fewer people migrating to urban/cities and a higher share of women (and their families) staying closer to home due to DBT income support, labour shortages will slowly begin to exert upward pressure on wages. This indeed means a fresh leg of demand-led volume growth in FMCG looks increasingly strong for years to come.

D2C Brands losing stream

On other hand, India’s once red-hot D2C(Direct to Consumer) startup ecosystem that emerged as a big competitor for FMCG giants in multiple categories, are now hitting a steep funding winter. According to Tracxn, total D2C investment fell to about $757 million in 2024, down 18% from $930 million in 2023 and a sharp 54% drop from the high of $1.6 billion in 2022. A recent post by founder of another popular D2C brand ‘Bombay Shaving Company’ shows how many of these D2C brands are now shutting down, getting sold for near-zero, founder CVs getting circulated.

“Every other day I hear of a new company with decent brand awareness, peak revenue of 7-8 Crores per month, good money raised but today is in a distress situation.”

- Shantanu Deshpande on Linkedin

This could very well be a temporary slow down in funding as well. While we do see successful D2C stories like Minimalist's acquisition by HUL in early 2025 as rare success story, which might also motivate more funds like L Catterton to put in more money funding the future of D2C brands in India, but that is expected to be more measured in the next funding wave, and could be more focused on creating new categories than just disrupting existing categories by simply burning cash. That next wave which could again become a headwind for existing FMCG giants in premium segments might be some distance away. Currently we are in consolidation phase of acquisitions & closures which might be best time for large FMCG companies to gain market share.

Also, the impact of D2C brands uprise is generally more in Tier 1 cities, subdued in Tier 2/3 and minimal in Tier 4 and rural areas, and it is indeed beyond Tier 1 geographies which we are more bullish on for coming years.

Look beyond Tier-1 Cities

All the government support and ever increasing incremental transfers (DBTs) we discussed till now in blog disproportionately benefit the public living in beyond Tier-1 cities, ie Tier 2/3/4 and rural. Building on what we discussed in our Part 1 on how estimated 80-85% of beneficiaries of this fresh Direct Income Transfers in multiple states are women residing in the rural India. As government continues to boost their expenditure in towards such benefits, they are directly boosting the consumption growth of rural India.

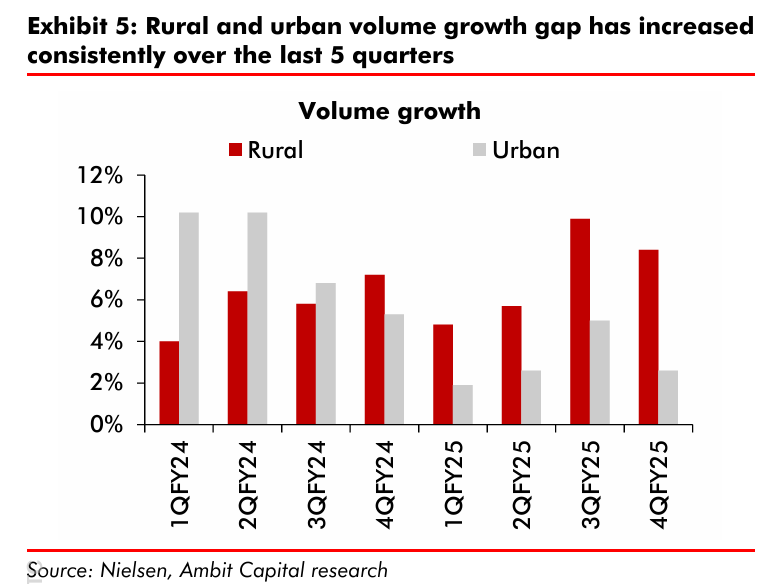

In the recent quarterly results, rural India has continued to emerge as a winner which higher growth. A consistent gap in favour of rural volumes may be an early signal of what sustained income support schemes and potential wage revival could unlock over a longer horizon. If DBTs continue expanding and wage pressures start to re-emerge after long time, rural India could be entering a mass consumption boom cycle.

So where are we betting? Time to reveal

Studies have shown that ‘women-led’ households spend very differently than ‘male-led’ households. Spending priorities change drastically.

Research, including financial diary studies by IIM Bangalore (Working Paper No. 484), shows that women-led households consistently spend more on food, hygiene, and child-related needs, while male-headed households often allocate more to fuel, entertainment, and more often on sin products like alcohol/cigarettes.

Even when borrowing from microfinance institutions, women tend to spend on essentials or small jewellery items that retain value, whereas men are more likely to direct funds toward appliances or non-essential purchases. This difference in financial behaviour has real implications for consumer-facing businesses. With rising balances of women bank accounts in country, there is now higher visibility that this income will flow into everyday consumption categories such as personal care, nutrition, and basic home products.

For FMCG companies, this could mean a more stable and scalable base for volume-led growth and rural premiumisation. Time to reveal our first major bet for next 3 to 5 years prospective.

Major Bet - Marico

Mass Market, Women centric Product Portfolio

Marico’s product portfolio is anchored by a strong mix of core and emerging categories, with hair oils and edible oils forming the bulk of its revenues. The company’s flagship brand Parachute Coconut Oil continues to be the single largest contributor, followed by Saffola, which includes a range of edible oils and oats under its healthy living umbrella. Together, the Parachute and Saffola franchises account for over 60 percent of Marico’s India revenue.

The next layer includes value-added hair oils (VAHO), where brands like Nihar and Hair & Care are positioned for scale in rural markets. Company is also building its foods portfolio, with Saffola Oats and Saffola Honey leading the charge in health-oriented snacking and kitchen staples.

This portfolio is a women centric portfolio - used in kitchen oils for cooking, personal care (hair oil), fast growing healthy food staple portfolio - we love it all! This is exactly what we aim to bet on.

Project SETU - Reach Deep in Rural

While everyone is focusing on just Quick Commerce in recent years, Marico is also focusing on an internal project named Project SETU where they plan to boost direct General Trade distribution from 1.0 million outlets in FY24 to 1.5 million by FY27, aiming to improve its Total to Direct Reach ratio from 5.8× to 4× in 3 years.

“Under SETU, we will focus on rural outlet expansion at a pan-India level, while deploying strong control frameworks to ensure sustainable outlet expansion across markets.”

- Saugata Gupta, MD & CEO, Marico (May, 2025 Q4 FY25 Concall)

Here their main aim is to deepen their rural penetration via improving direct rural distribution network by leveraging digitisation, data-led targeting, and last-mile delivery models. They also aim to get this to urban areas like Tier 2/3/4 to increase their offline retail reach. This will benefit hair oils & food staple portfolio and help them diversify away from Parachute coconut oil.

Focusing more on offline distribution is again a right long term move - deeper in rural penetration they go, more confident we get on this bet.

Minor Bet - Avenue Supermart (Dmart)

Retail story in last 3 years in Financial Year 2023, 2024, and 2025 has overly focused on disruption by Quick Commerce and has somehow believed Dmart is getting defeated in the retail game it mastered before.

While these years have indeed been years of reckoning for the company, as it became clear that the Quick Commerce model is here to stay and is steadily drawing away its affluent customers in metro cities, the company appears to have made a strategic shift to focus more on Tier 2/3/4 regions.

Recently from April to June 2025 period, company opened 9 stores in cities: Kamrej, Mandya, Rewa, Malad East, Phagwara, Agra, Tiruvallur, Chhindwara & Ankhol - Almost all these cities are non-metro areas, where value focused consumers density is highest. Company has also entered in Uttar Pradesh finally and would plan to expand rapidly there as well.

At the time of its IPO in 2017, the company had 118 stores, which has now increased to 440. This means that around 70 percent of its total store count was added between 2017 and 2025, a period when FMCG demand was relatively subdued due to weak wage growth among the mass market, as discussed before. As this trend begins to reverse, these stores may witness stronger-than-anticipated volume growth in the years ahead. A big consumption wave by masses/value conscious customer could be brewing in next few years and Modern Trade will continue be a bigger portion of the total FMCG sales.

Closing remarks

India’s consumption story is entering a new phase, one that will be shaped not by premium urban demand, but by steady, broad-based rural uplift, especially led by women. What began as a political strategy through direct transfers is now manifesting as structural shifts in household spending, rural wage formation, and the kind of products being consumed.

We are bullish on this new upcoming consumption wave and are playing it via stocks named Marico & Avenue Supermart (DMart) - This blog is not investment advice, nor are we SEBI-registered advisors. Kindly refer to the disclosures below.

We hope you enjoyed reading this blog. Please give feedback by leaving a comment below and share this blog further if you find it valuable.

You can reach out to us on LinkedIn here: Aditya Grover & Kinjal Karwa

Finding Outperformers will always remain a free-to-access website. If you find our work valuable, consider supporting our team by contributing to our research here:

Read our recent publications here:

India’s Labour Advantage is Slipping

Back in June 2024, Larsen & Toubro (L&T) revealed it was facing a severe shortage of over 45,000 workers across its operations, including 25,000–30,000 labourers in its construction division. Multiple factors were at play, including extreme weather (rains), disruptions due to elections, and other logistical challenges.

Disclaimers-

We are not a SEBI registered advisors; personal investment/interest in shares can exists for any company mentioned above; this isn’t investment advice but our personal thought process; DYOR (do your own research) is recommended; Investing & trading are subject to market risk; the decision maker is responsible for any outcome.

| A guest post by

|

Why only Marico? There are other FMCG companies like HUL, ITC having diversified products at affordable price points with tremendous reach in semi urban and rural areas.

Bhulekh MP is a helpful digital portal that provides easy access to land records in Madhya Pradesh. It allows citizens to check ownership details, khasra, khatauni, and maps online, saving both time and effort. This platform promotes transparency in land management and reduces the chances of disputes. https://mplandrecord.net/